Collinearity: Impact and Possible Remedies

Deepayan Sarkar

What is collinearity?

Exact dependence between columns of \(\mathbf{X}\) make coefficients non-estimable

Collinearity refers to the situation where some columns are almost dependent

Why is this a problem?

Individual coefficient estimates \(\hat{\beta}_j\) become unstable (high variance)

Standard errors are large, tests have low power

On the other hand, \(\hat{\mathbf{y}} = \mathbf{H} \mathbf{y}\) is not particularly affected

Detecting collinearity

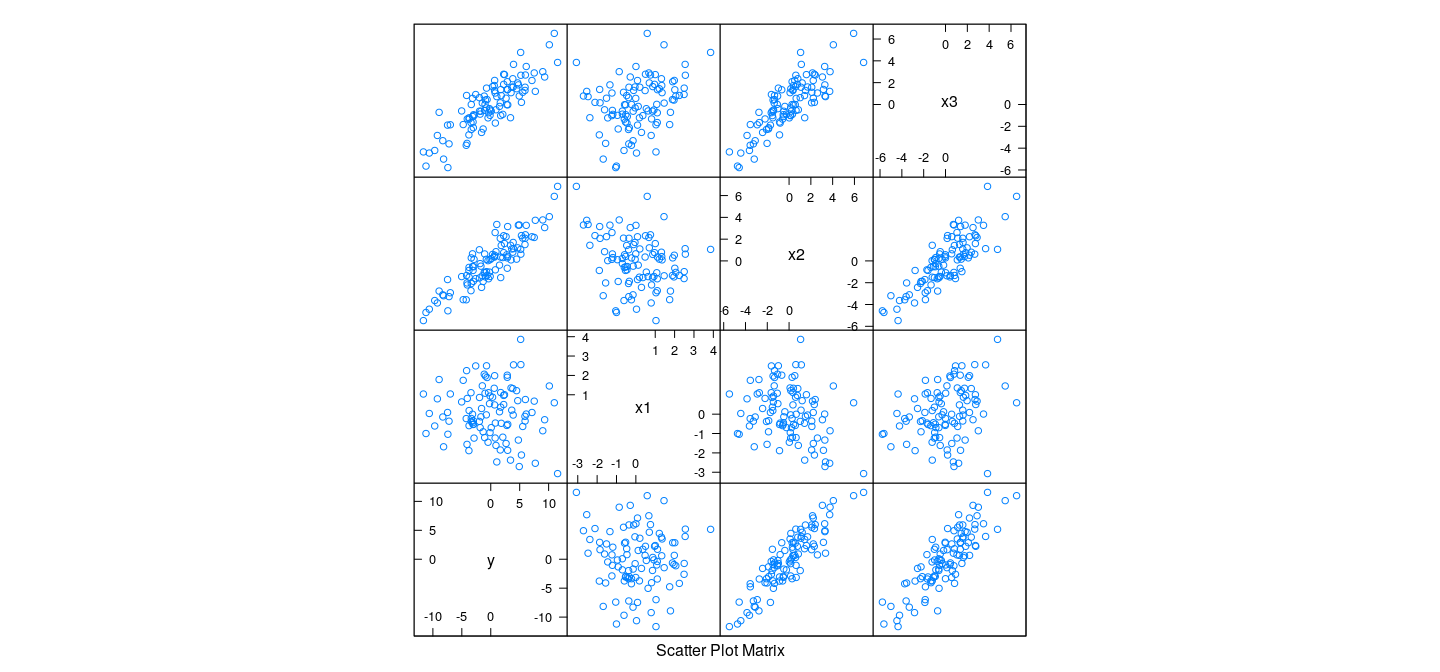

Collinearity in pairs of variables are easily seen in scatter plots

However, higher dimensional collinearity may not be readily apparent

Example:

n <- 100

z1 <- rnorm(n)

z2 <- rnorm(n)

x1 <- z1 + z2 + 0.1 * rnorm(n)

x2 <- z1 - 2 * z2 + 0.1 * rnorm(n)

x3 <- 2 * z1 - z2 + 0.1 * rnorm(n)

y <- x1 + 2 * x2 + 2 * rnorm(n) # x3 has coefficient 0

d3 <- data.frame(y, x1, x2, x3)

cor(d3) y x1 x2 x3

y 1.00000000 -0.05350867 0.8930301 0.8498399

x1 -0.05350867 1.00000000 -0.2750082 0.3047524

x2 0.89303013 -0.27500823 1.0000000 0.8287638

x3 0.84983991 0.30475236 0.8287638 1.0000000Detecting collinearity

Detecting collinearity

- In this case, a 3-D plot is sufficient (but not enough for higher-dimensional collinearity)

Detecting collinearity

Pairwise scatter plots do not indicate unusual dependence

However, each \(X_{* j}\) is highly dependent on others

[1] 0.9816998[1] 0.9936826[1] 0.9938004Impact of collinearity

- This results in increased uncertainty in coefficient estimates

Call:

lm(formula = y ~ x1 + x2 + x3, data = d3)

Residuals:

Min 1Q Median 3Q Max

-4.5620 -1.3326 -0.0007 1.6717 4.5924

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.04719 0.20629 0.229 0.8195

x1 1.09743 1.12399 0.976 0.3313

x2 2.38916 1.12119 2.131 0.0357 *

x3 -0.33411 1.12900 -0.296 0.7679

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 2.042 on 96 degrees of freedom

Multiple R-squared: 0.8376, Adjusted R-squared: 0.8325

F-statistic: 165 on 3 and 96 DF, p-value: < 2.2e-16

- Even though overall regression is highly significant, individual predictors are (marginally) not

Impact of collinearity

- The situation changes dramatically if any one of the predictors is dropped

Call:

lm(formula = y ~ x2 + x3, data = d3)

Residuals:

Min 1Q Median 3Q Max

-4.8389 -1.3677 0.0208 1.7567 4.4134

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.07408 0.20439 0.362 0.718

x2 1.30556 0.15921 8.200 1.01e-12 ***

x3 0.75725 0.15882 4.768 6.54e-06 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 2.041 on 97 degrees of freedom

Multiple R-squared: 0.836, Adjusted R-squared: 0.8326

F-statistic: 247.1 on 2 and 97 DF, p-value: < 2.2e-16Impact of collinearity

- The correct model (dropping

x3, whose true coefficient is 0) performs equally well (not better)

Call:

lm(formula = y ~ x1 + x2, data = d3)

Residuals:

Min 1Q Median 3Q Max

-4.6542 -1.3492 0.0212 1.7051 4.5374

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.05486 0.20369 0.269 0.788

x1 0.76811 0.15740 4.880 4.16e-06 ***

x2 2.05850 0.09225 22.314 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 2.032 on 97 degrees of freedom

Multiple R-squared: 0.8374, Adjusted R-squared: 0.8341

F-statistic: 249.8 on 2 and 97 DF, p-value: < 2.2e-16Impact of collinearity

- The difference is reflected in the estimated variance-covariance matrix of \(\hat\beta\)

x1 x2 x3

x1 1.0000000 0.9898617 -0.9900518

x2 0.9898617 1.0000000 -0.9965770

x3 -0.9900518 -0.9965770 1.0000000 x1 x2

x1 1.0000000 0.2750082

x2 0.2750082 1.0000000Impact of collinearity

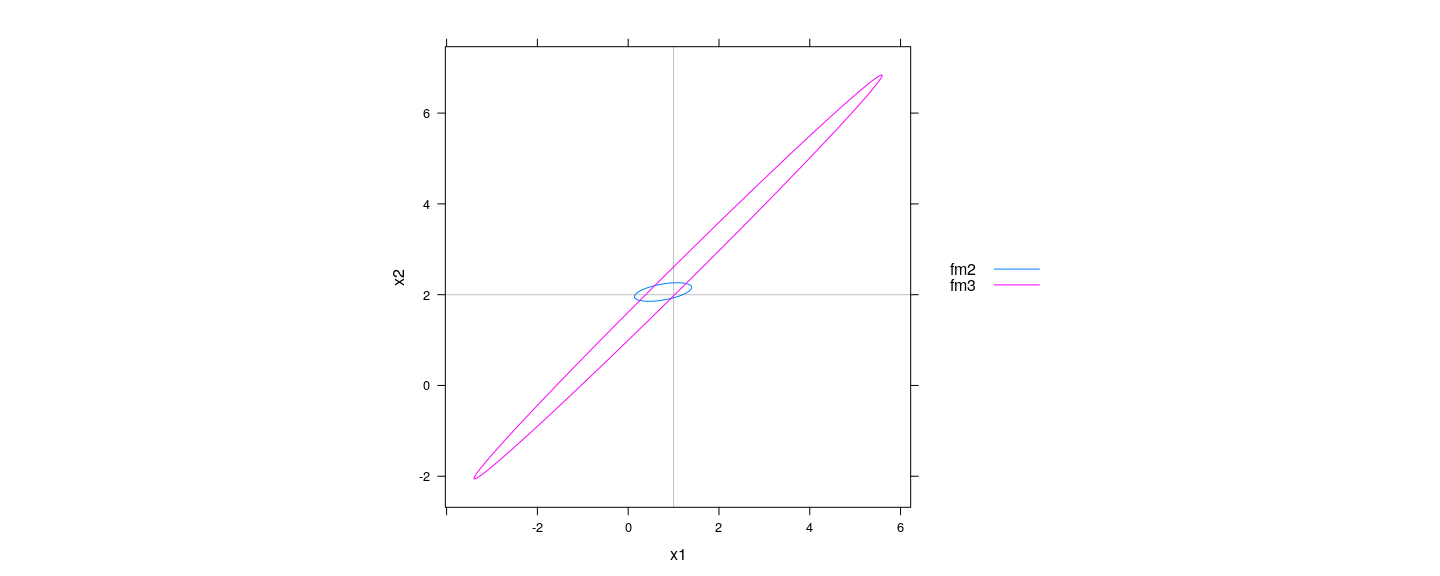

- The situation is more clearly seen in the confidence ellipsoids for \(\hat\beta\)

C3 <- chol(vcov(fm3)[2:3, 2:3]) # only x1 and x2

C2 <- chol(vcov(fm2)[2:3, 2:3])

tt <- seq(0, 1, length.out = 101)

circle <- rbind(2 * cos(2 * pi * tt), sin(2 * pi * tt))

E3 <- coef(fm3)[2:3] + 2 * t(C3) %*% circle

E2 <- coef(fm2)[2:3] + 2 * t(C2) %*% circle

E <- as.data.frame(rbind(t(E2), t(E3))); E$model <- rep(c("fm2", "fm3"), each = 101)Impact of collinearity

xyplot(x2 ~ x1, data = E, groups = model, abline = list(v = 1, h = 2, col = "grey"), type = "l",

aspect = "iso", auto.key = list(lines = TRUE, points = FALSE, space = "right"))

- Many different \((\beta_1, \beta_2, \beta_3)\) combinations give essentially equivalent fit

Variance inflation factor

- It can be shown that the sampling variance of \(\hat{\beta}_j\) is

\[ V( \hat{\beta}_j ) = \sigma^2 (\mathbf{X}^T \mathbf{X})^{-1}_{jj} = \frac{1}{1-R_j^2} \times \frac{\sigma^2}{(n-1) s_j^2} \]

where

\(s_j^2 = \frac{1}{n-1} \sum_i (X_{ij} - \bar{X}_j)^2\) (sample variance of \(X_{* j}\))

\(R_j^2\) is the multiple correlation coefficient of \(X_{* j}\) on the remaining columns of \(\mathbf{X}\)

Variance inflation factor

- The Variance Inflation Factor (VIF) is defined as

\[ VIF_j = \frac{1}{1-R_j^2} \]

\(VIF_j\) directly reflects the effect of collinearity on the precision of \(\hat{\beta}_j\)

Length of the confidence interval for \(\hat{\beta}_j\) is proportional to \(\sqrt{V(\hat{\beta}_j)}\), so more useful to compare \(\sqrt{VIF_j}\)

x1 x2 x3

7.392177 12.581416 12.700439 x1 x2

1.040104 1.040104 Variance inflation factor

- For a more intuitive justification, recall partial regression of

- residuals from regression of \(\mathbf{y}\) on \(\mathbf{X}_{(-j)}\), and

- residuals from regression of \(\mathbf{X}_{*j}\) on \(\mathbf{X}_{(-j)}\)

\(\hat{\beta}_j\) from this partial regression is the same as \(\hat{\beta}_j\) from the full model

In presence of collinearity, residuals from regression of \(\mathbf{X}_{*j}\) on \(\mathbf{X}_{(-j)}\) will have very low variability

[1] 2.308524[1] 0.1817672Variance inflation factor

- Resulting \(\hat{\beta}_j\) is highly unstable

Coping with collinearity

There is no real solution if we want to estimate individual coefficients

Recall interpretation of \(\beta_j\): increase in \(E(y)\) for unit increase in \(x_j\) keeping other covariates fixed

For collinear data, this cannot be reliably estimated

However, there are several approaches to “stabilize” the model

Approaches to deal with collinearity

Variable selection:

- Use criteria such as AIC and BIC in conjunction with stepwise / all-subset search

- As discussed earlier, this is usually a misguided approach

- In presence of collinearity, choice of model very sensitive to random error

Respecify model: perhaps combine some predictors

- Principal component analysis (PCA):

- An automated version of model respecification

- Linearly transform covariates to make them orthogonal

- Reduce dimension of covariate space by dropping “unimportant” variables

Penalized regression:

- Add some sort of penalty for “unlikely” estimates of \(\beta\) (e.g., many large components)

- This is essentially a Bayesian approach

- Results in biased estimates, but usually much more stable

- For certain kinds of penalties, also works well as a variable selection mechanism

Standardization

We will briefly discuss principal components and penalized regression

Both these approaches have a practical drawback: they are not invariant to variable rescaling

Recall that for linear regression, location-scale changes of covariates does not change fitted model

This is no longer true if we used PCA or penalized regression

There is no real solution to this problem: usual practice is to standardize all covariates

Specifically, subtract mean, divide by standard deviation (so covariates have mean 0, variance 1)

For prediction, the same scaling must be applied to new observations

Can use R function

scale()which also returns mean and SD for subsequent useMore details later as necessary

Principal components

Will be studies in more details in Multivariate Analysis course

In what follows, the intercept is not considered as a covariate

Let \(\mathbf{z}_j\) denote the \(j\)-th covariate (column on \(\mathbf{X}\)) after standardization

This means that the length of each \(\mathbf{z}_j\) is \(\lVert \mathbf{z}_j \rVert = \sqrt{\sum_i z_{ij}^2} = n-1\)

This is not necessary for PCA, but is usually not meaningful

Consider the matrix \(\mathbf{Z} = [ \mathbf{z}_1 \, \mathbf{z}_2 \, \cdots \, \mathbf{z}_k ]\)

Suppose the rank of \(\mathbf{Z}\) is \(p\); for our purposes, \(p = k\)

Principal components

Our goal is to find \(\mathbf{W} = [ \mathbf{w}_1 \, \mathbf{w}_2 \, \cdots \, \mathbf{w}_p ] = \mathbf{Z} \mathbf{A}\) such that

\({\mathcal C}(\mathbf{W}) = {\mathcal C}(\mathbf{Z})\)

Columns of \(\mathbf{W}\) are mutually orthogonal

The first principal component \(\mathbf{w}_1\) has the largest variance among linear combinations of columns of \(\mathbf{Z}\)

The second principal component \(\mathbf{w}_2\) has the largest variance among linear combinations of columns of \(\mathbf{Z}\) that are orthogonal to \(\mathbf{w}_1\)

… and so on

More precisely, we only consider normalized linear combinations \(\mathbf{Z} \mathbf{a}\) such that \(\lVert \mathbf{a} \rVert^2 = \mathbf{a}^T \mathbf{a} = 1\)

Otherwise, the variance of \(\mathbf{Z} \mathbf{a}\) can be made arbitrarily large

Principal components

Note that by construction any linear combination of \(\mathbf{z}_1, \mathbf{z}_2, \dotsc, \mathbf{z}_k\) has mean 0

The variance of any such \(\mathbf{w} = \mathbf{Z} \mathbf{a}\) is given by

\[ s^2(\mathbf{a}) = \frac{1}{n-1} \mathbf{w}^T \mathbf{w} = \frac{1}{n-1} \mathbf{a}^T \mathbf{Z}^T \mathbf{Z} \mathbf{a} = \mathbf{a}^T \mathbf{R} \mathbf{a} \]

where \(\mathbf{R} = \frac{1}{n-1} \mathbf{Z}^T \mathbf{Z}\) is the correlation matrix of the original predictors \(\mathbf{X}\)

We can maximize \(s^2(\mathbf{a})\) subject to the constraint \(\mathbf{a}^T \mathbf{a} = 1\) using a Lagrange multiplier:

\[ F = \mathbf{a}^T \mathbf{R} \mathbf{a} - \lambda (\mathbf{a}^T \mathbf{a} - 1) \]

Principal components

- Differentiating w.r.t. \(\mathbf{a}\) and \(\lambda\) and equating to 0, we get

- In other words, potential solutions are the normalized eigenvectors of \(\mathbf{R}\)

Which of these \(k\) solutions maximizes \(s^2(\mathbf{a})\)?

For any solution \(\mathbf{a}\), the variance \(s^2(\mathbf{a}) = \mathbf{a}^T \mathbf{R} \mathbf{a} = \lambda\, \mathbf{a}^T \mathbf{a} = \lambda\)

So the first principal component is given by the eigenvector \(\mathbf{a}_1\) corresponding to the largest eigenvalue \(\lambda_1\)

Principal components

Let the eigenvalues in decreasing order be \(\lambda_1 \geq \lambda_2 \geq \cdots \geq \lambda_k\)

Not surprisingly, the principal components are given by the corresponding eigenvectors \(\mathbf{a}_1, \mathbf{a}_2, \dotsc, \mathbf{a}_k\)

The desired transformation matrix \(\mathbf{A}\) is given by \(\mathbf{A} = [ \mathbf{a}_1 \, \mathbf{a}_2 \, \cdots \, \mathbf{a}_k ]\)

As the eigenvectors are normalized, \(\mathbf{A}^T \mathbf{A} = \mathbf{I}\)

The variance-covariance matrix of the principal components \(\mathbf{W}\) is

\[ \frac{1}{n-1} \mathbf{W}^T \mathbf{W} = \frac{1}{n-1} \mathbf{A}^T \mathbf{Z}^T \mathbf{Z} \mathbf{A} = \mathbf{A}^T \mathbf{R} \mathbf{A} = \mathbf{A}^T \mathbf{A} \mathbf{\Lambda} = \mathbf{\Lambda} \]

- Here \(\mathbf{\Lambda}\) is the diagonal matrix with entries \(\lambda_1, \lambda_2, \dotsc, \lambda_k\)

Principal components

- A general indicator of the degree of collinearity present in the covariates is the condition number

\[ K \equiv \sqrt{\frac{\lambda_1}{\lambda_k}} \]

- Large condition number indicates that small changes in data can cause large changes in \(\hat{\beta}\)

In theory, using (all) principal components as covariates leads to the same fit (i.e., same \(\mathbf{H}\), \(\hat{\mathbf{y}}\), etc.)

To “stabilize” collinearity, we can instead regress on the first few principal components

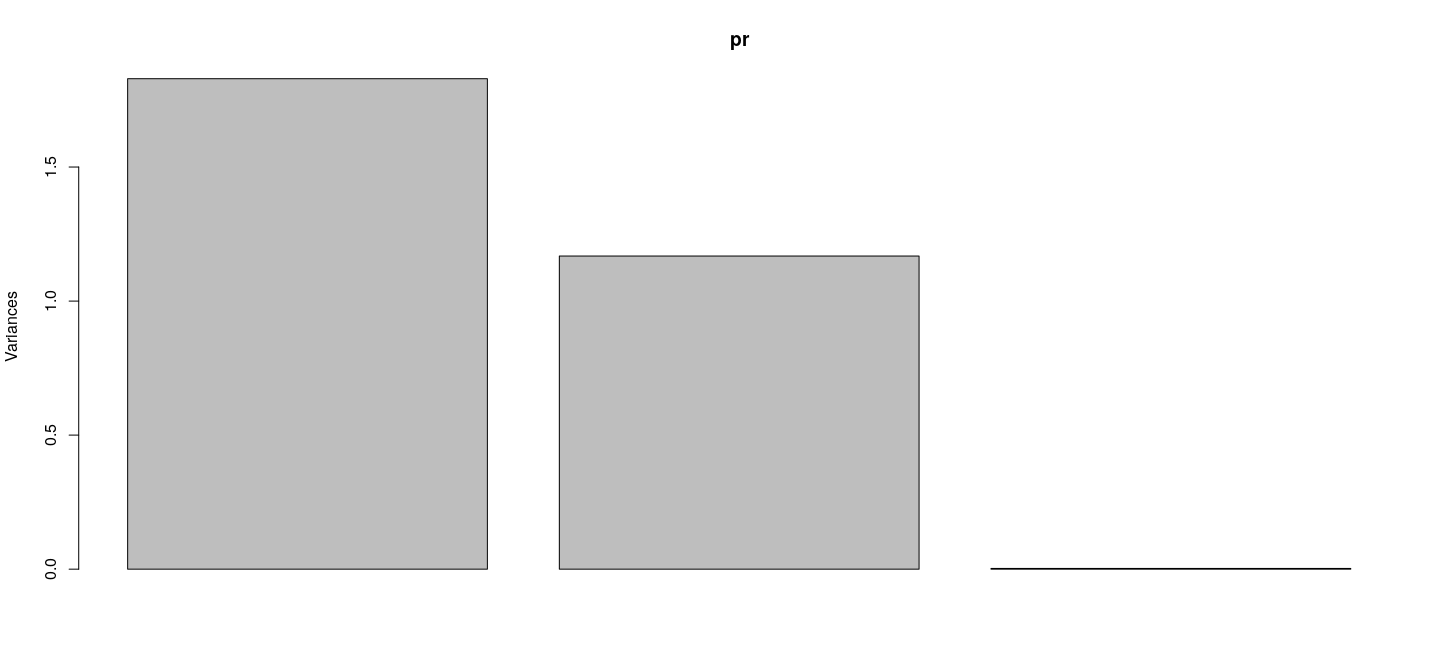

Principal components in R

Standard deviations (1, .., p=3):

[1] 1.35254256 1.08071572 0.05178952

Rotation (n x k) = (3 x 3):

PC1 PC2 PC3

x1 -0.02887707 -0.9244271 0.3802640

x2 -0.70174549 0.2896624 0.6508832

x3 -0.71184225 -0.2480529 -0.6570771 PC1 PC2 PC3

1 1.1023871 -0.0005434015 0.072144023

2 0.1583731 -1.9368798962 -0.023836194

3 -0.8266643 -0.1014248304 -0.088178195

4 0.3620938 0.6099882730 -0.020273616

5 1.2346433 0.2956850245 -0.023914456

6 1.7477325 1.2684577099 -0.002962102Principal components in R: scree plot

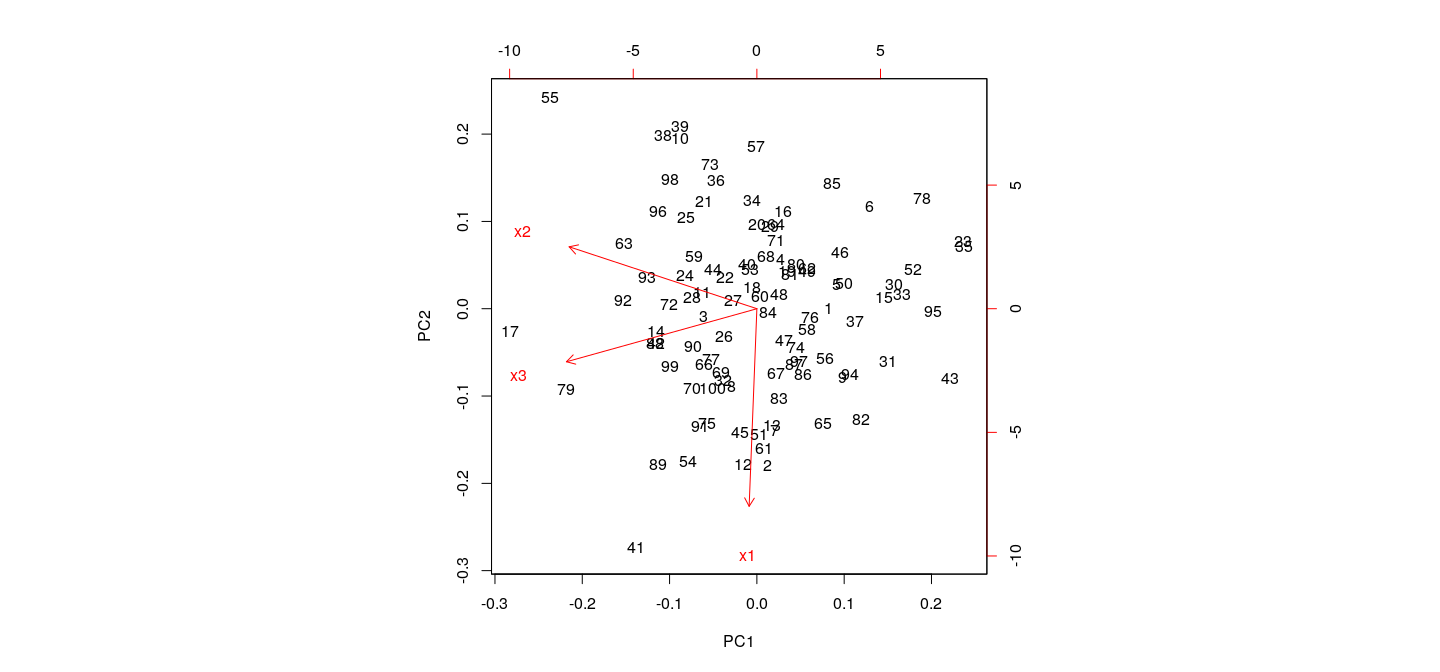

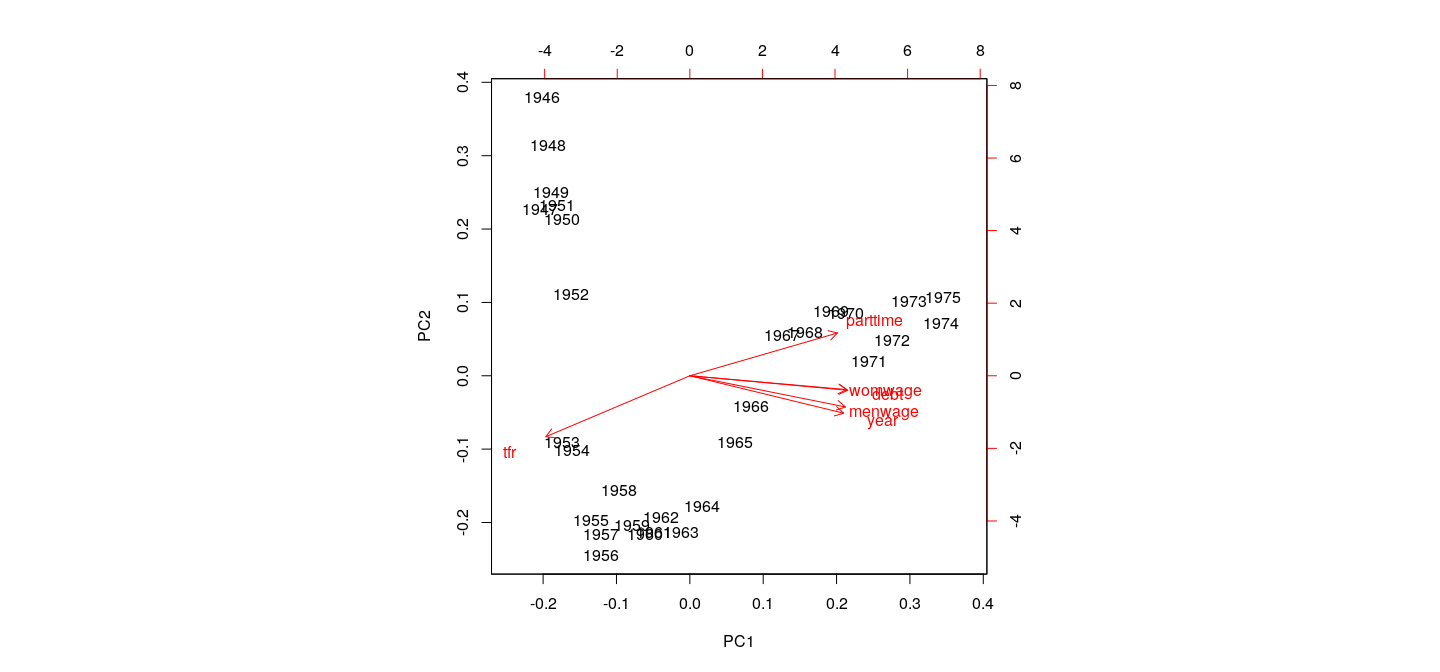

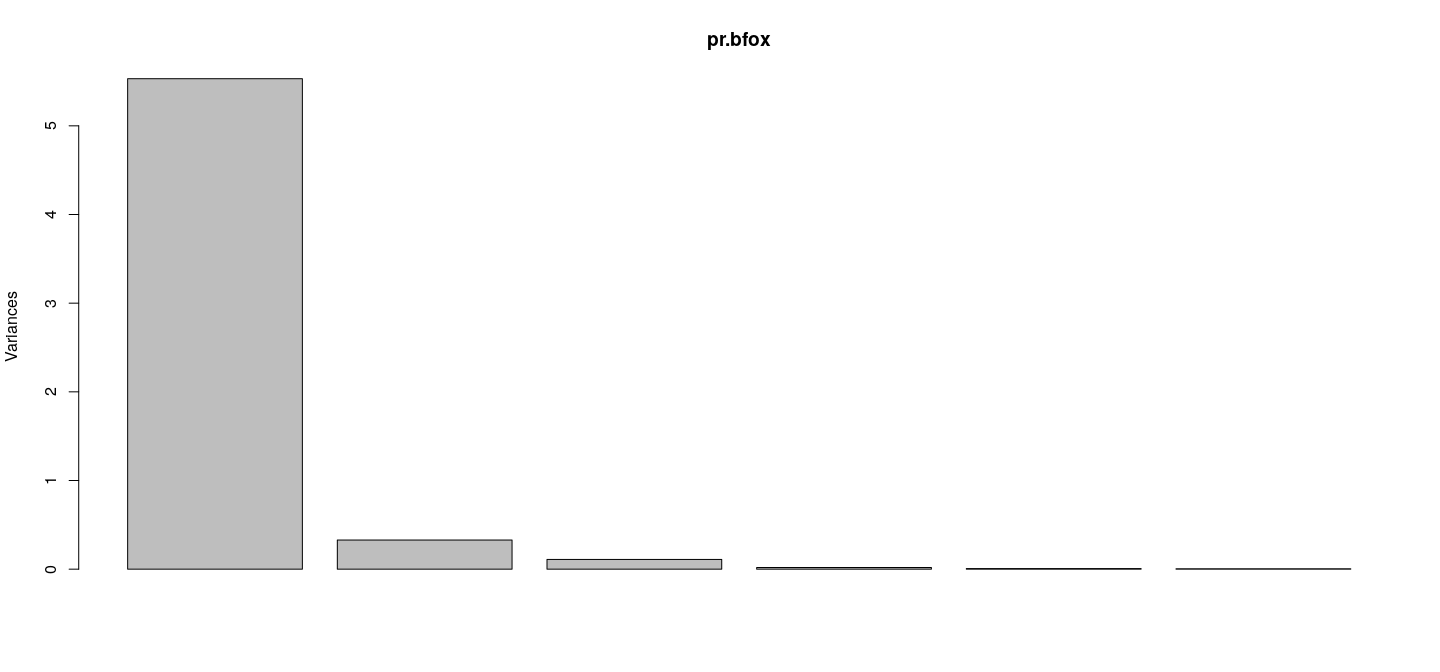

Principal components in R: biplot

Principal components are orthogonal

Principal component regression

Call:

lm(formula = y ~ PC1 + PC2 + PC3, data = d3)

Residuals:

Min 1Q Median 3Q Max

-4.5620 -1.3326 -0.0007 1.6717 4.5924

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.04883 0.20419 0.239 0.811

PC1 -3.35460 0.15173 -22.110 <2e-16 ***

PC2 0.41578 0.18989 2.190 0.031 *

PC3 4.65106 3.96249 1.174 0.243

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 2.042 on 96 degrees of freedom

Multiple R-squared: 0.8376, Adjusted R-squared: 0.8325

F-statistic: 165 on 3 and 96 DF, p-value: < 2.2e-16 (Intercept) PC1 PC2 PC3

(Intercept) 0.041692 0.000000 0.000000 0.00000

PC1 0.000000 0.023021 0.000000 0.00000

PC2 0.000000 0.000000 0.036058 0.00000

PC3 0.000000 0.000000 0.000000 15.70134Principal component regression

Call:

lm(formula = y ~ PC1 + PC2, data = d3)

Residuals:

Min 1Q Median 3Q Max

-4.9339 -1.3878 0.0018 1.7533 4.3695

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.04883 0.20458 0.239 0.8118

PC1 -3.35460 0.15202 -22.067 <2e-16 ***

PC2 0.41578 0.19026 2.185 0.0313 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 2.046 on 97 degrees of freedom

Multiple R-squared: 0.8352, Adjusted R-squared: 0.8318

F-statistic: 245.9 on 2 and 97 DF, p-value: < 2.2e-16 (Intercept) PC1 PC2

(Intercept) 0.04185465 0.00000000 0.00000000

PC1 0.00000000 0.02311036 0.00000000

PC2 0.00000000 0.00000000 0.03619809Statistical interpretation of Principal Component regression

PCA rotates (through \(\mathbf{A}\)) and scales (through \(\mathbf{\Lambda}\)) \(\mathbf{Z}\) to make columns orthonormal

Resulting variables may be thought of as “latent variables” controlling observed covariates

Principal components with higher variability lead to smaller sampling variance of coefficients

Orthogonality means that estimated coefficients are uncorrelated

Unfortunately, no longer possible to interpret effect of individual covariates

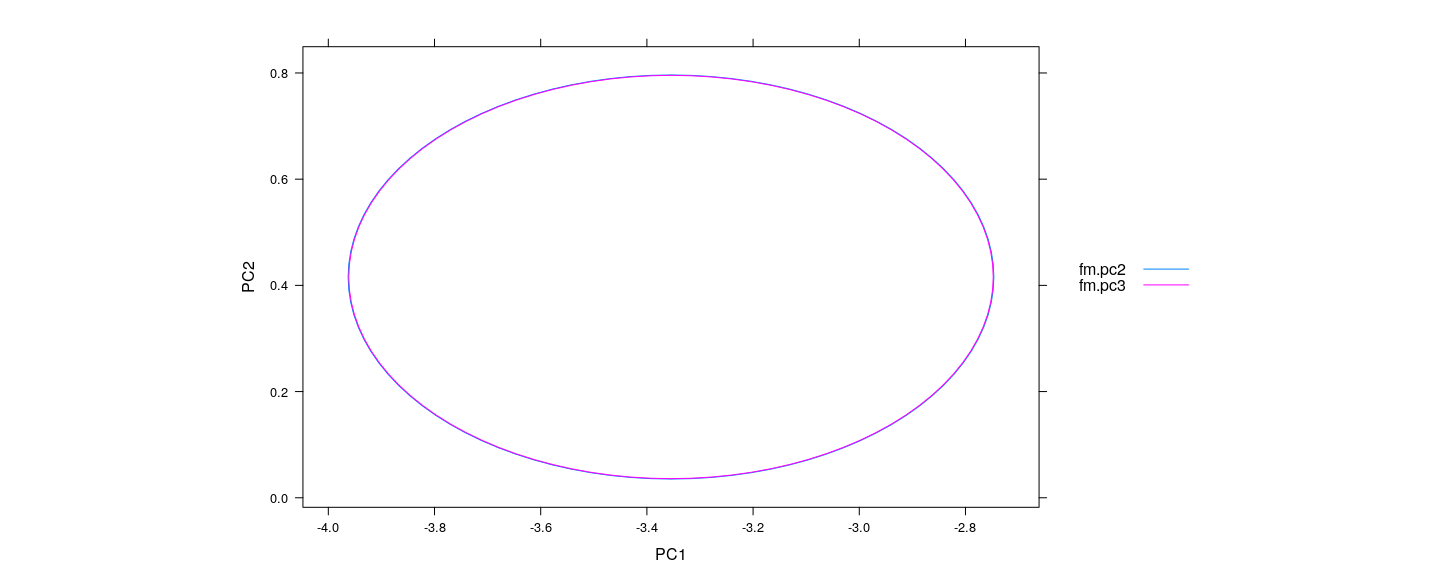

- Confidence ellipsoids are essentially identical (except for different residual d.f.)

C3 <- chol(vcov(fm.pc3)[2:3, 2:3]) # only PC1 and PC2

C2 <- chol(vcov(fm.pc2)[2:3, 2:3])

tt <- seq(0, 1, length.out = 101)

circle <- rbind(2 * cos(2 * pi * tt), sin(2 * pi * tt))

E3 <- coef(fm.pc3)[2:3] + 2 * t(C3) %*% circle

E2 <- coef(fm.pc2)[2:3] + 2 * t(C2) %*% circle

E.pc <- as.data.frame(rbind(t(E2), t(E3))); E.pc$model <- rep(c("fm.pc2", "fm.pc3"), each = 101)Confidence ellipsoids in principal component regression

xyplot(PC2 ~ PC1, data = E.pc, groups = model, abline = list(v = 1, h = 2, col = "grey"), type = "l",

aspect = "iso", auto.key = list(lines = TRUE, points = FALSE, space = "right"))

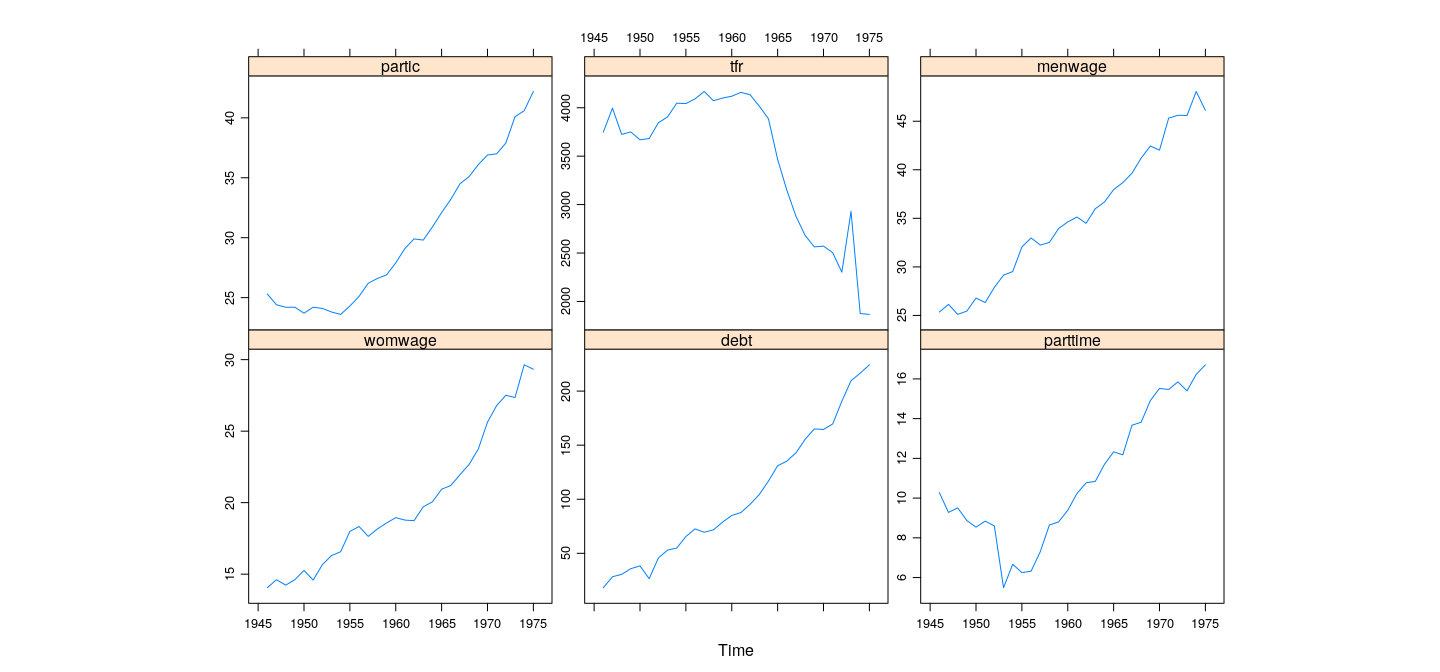

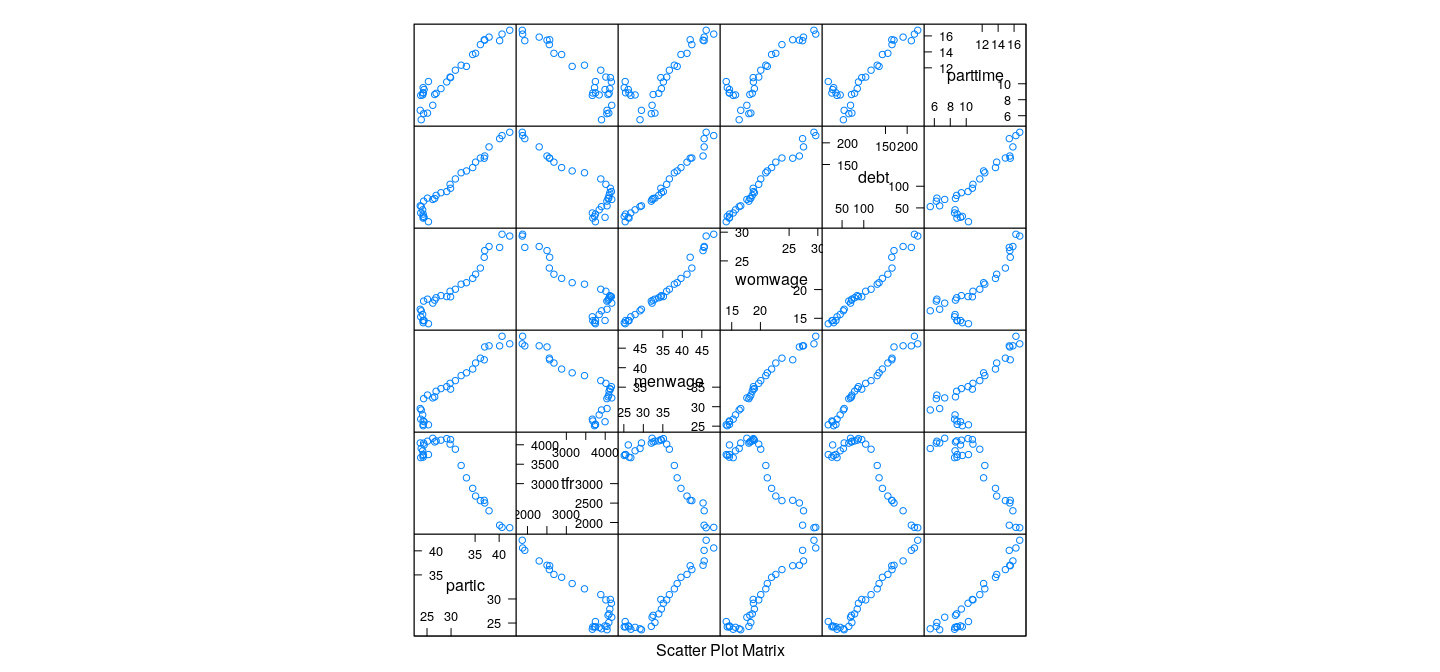

Example: Canadian Women’s Labour-Force Participation

Example: Canadian Women’s Labour-Force Participation

Example: Canadian Women’s Labour-Force Participation

Call:

lm(formula = partic ~ ., data = Bfox)

Residuals:

Min 1Q Median 3Q Max

-0.83213 -0.33438 -0.01621 0.36769 1.05048

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 8.142e+00 2.129e+02 0.038 0.96982

tfr -1.949e-06 5.011e-04 -0.004 0.99693

menwage -2.919e-02 1.502e-01 -0.194 0.84766

womwage 1.984e-02 1.744e-01 0.114 0.91041

debt 6.397e-02 1.850e-02 3.459 0.00213 **

parttime 6.566e-01 8.205e-02 8.002 4.27e-08 ***

year 4.452e-03 1.107e-01 0.040 0.96827

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.5381 on 23 degrees of freedom

Multiple R-squared: 0.9935, Adjusted R-squared: 0.9918

F-statistic: 587.3 on 6 and 23 DF, p-value: < 2.2e-16Example: Canadian Women’s Labour-Force Participation

tfr menwage womwage debt parttime year

3.891829 10.673117 8.205214 11.474235 2.748158 9.755120 Standard deviations (1, .., p=6):

[1] 2.35180659 0.57341995 0.33183302 0.13614037 0.08403192 0.06698201

Rotation (n x k) = (6 x 6):

PC1 PC2 PC3 PC4 PC5 PC6

tfr -0.3849387 -0.6675739 0.54244962 0.2518053 0.19660094 0.09928673

menwage 0.4158879 -0.3420846 -0.02228191 0.1571042 -0.70548213 0.43258778

womwage 0.4195650 -0.1523080 -0.26579808 0.7291795 0.27909187 -0.34716538

debt 0.4220132 -0.1591200 -0.09747758 -0.2757411 0.61883636 0.57279338

parttime 0.3945669 0.4692796 0.77462008 0.1520461 0.02516761 0.01748999

year 0.4111526 -0.4105886 0.15831978 -0.5301495 -0.04646405 -0.59505293

Example: Canadian Women’s Labour-Force Participation

All variables contribute roughly equally to first PC

Note non-linear pattern (PCA only accounts for linear relationships)

Example: Canadian Women’s Labour-Force Participation

- First PC explains bulk of the variability (92%)

Example: Canadian Women’s Labour-Force Participation

Call:

lm(formula = partic ~ PC1 + PC2 + PC3 + PC4 + PC5 + PC6, data = Bfox)

Residuals:

Min 1Q Median 3Q Max

-0.83213 -0.33438 -0.01621 0.36769 1.05048

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 29.99667 0.09823 305.356 < 2e-16 ***

PC1 2.50998 0.04248 59.080 < 2e-16 ***

PC2 0.44179 0.17424 2.535 0.018485 *

PC3 1.30075 0.30110 4.320 0.000254 ***

PC4 -0.74497 0.73391 -1.015 0.320632

PC5 2.67915 1.18900 2.253 0.034079 *

PC6 2.16416 1.49166 1.451 0.160326

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.5381 on 23 degrees of freedom

Multiple R-squared: 0.9935, Adjusted R-squared: 0.9918

F-statistic: 587.3 on 6 and 23 DF, p-value: < 2.2e-16