Diagnosing Systematic Model Violations

Deepayan Sarkar

Violation of assumptions in a linear regression model

Systematic violations

- Non-normality of errors

- Nonconstant error variance

- Lack of fit (nonlinearity)

- (Autocorrelation in errors — later)

Non-normality of errors

- Why do we care? LSE is Best Linear Unbiased Estimator under assumptions of

- linearity

- constant variance

- uncorrelated errors

Even if LSE is valid, it may not be efficient, especially with heavy tailed errors (outliers)

LSE estimates conditional mean \(f(x) = E(Y | X = x)\)

Multimodal error distribution usually indicates presense of latent covariate

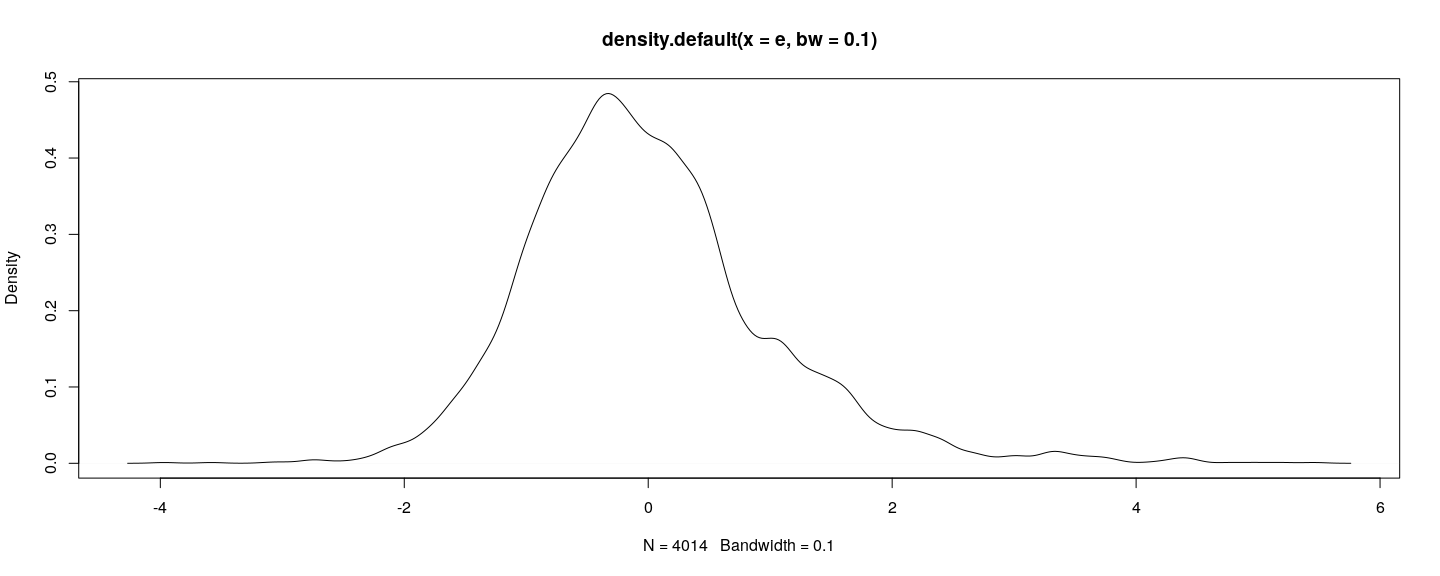

Graphical techniques

Although formal tests exist, we will focus on graphical techniques

More useful in practice because they can pinpoint nature of violation

![plot of chunk unnamed-chunk-1]()

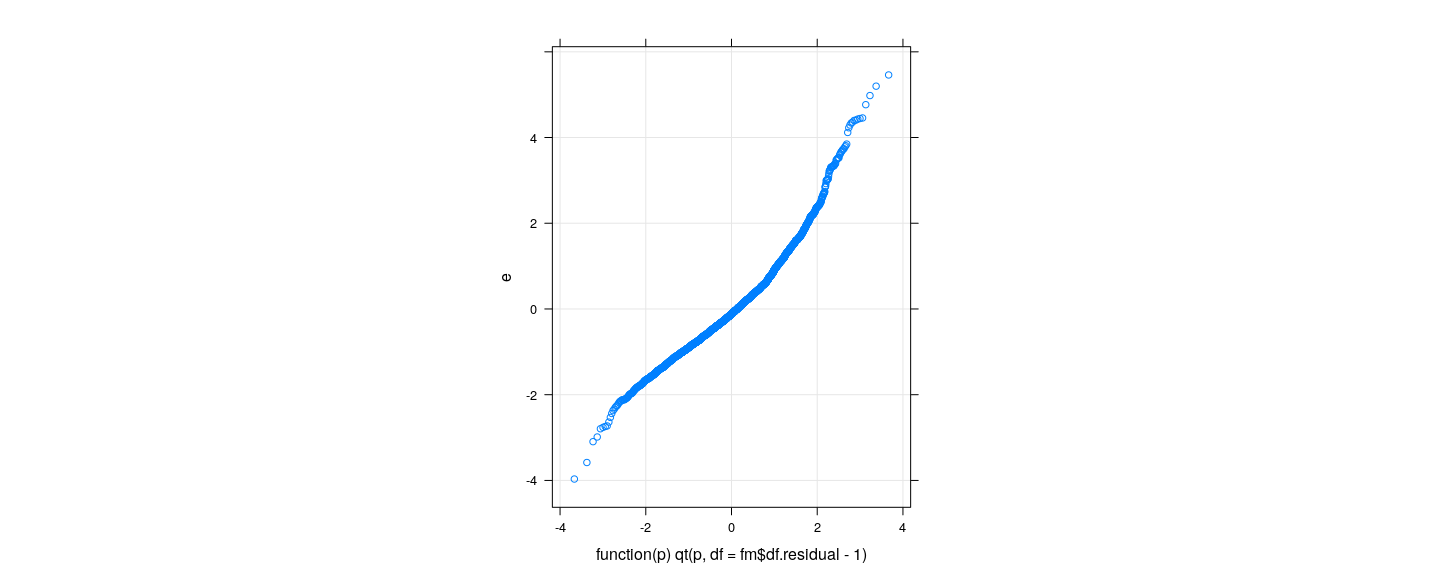

Graphical techniques

![plot of chunk unnamed-chunk-2]()

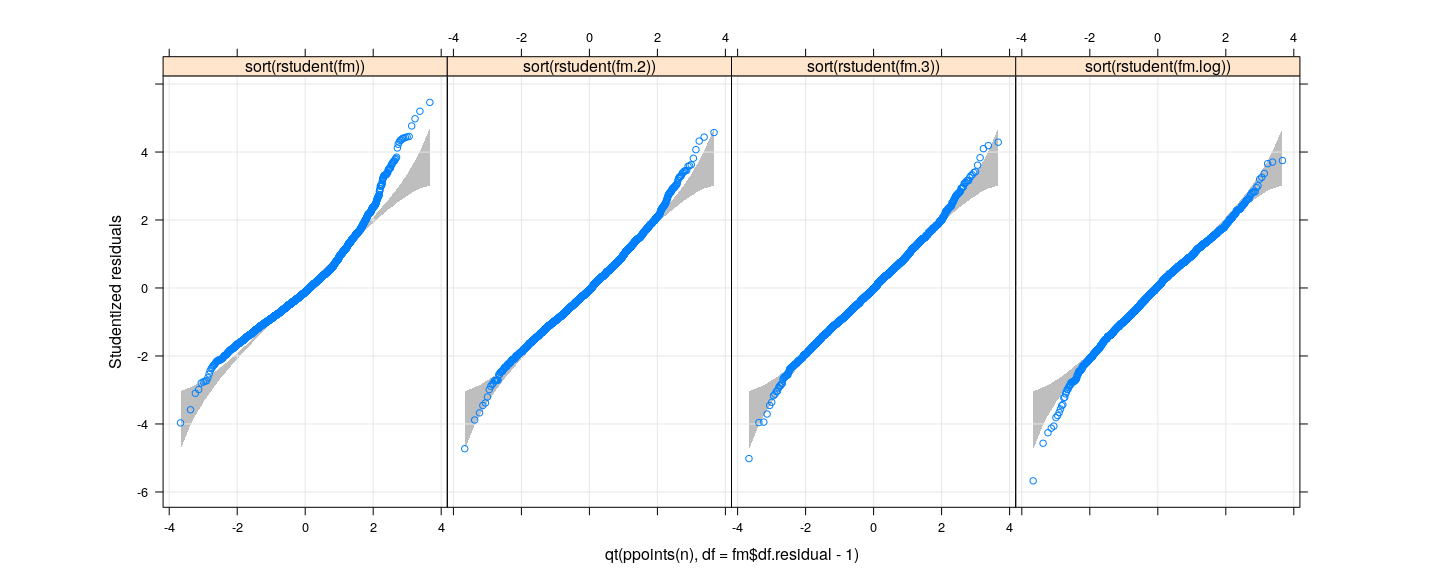

- But is there a reference to compare to?

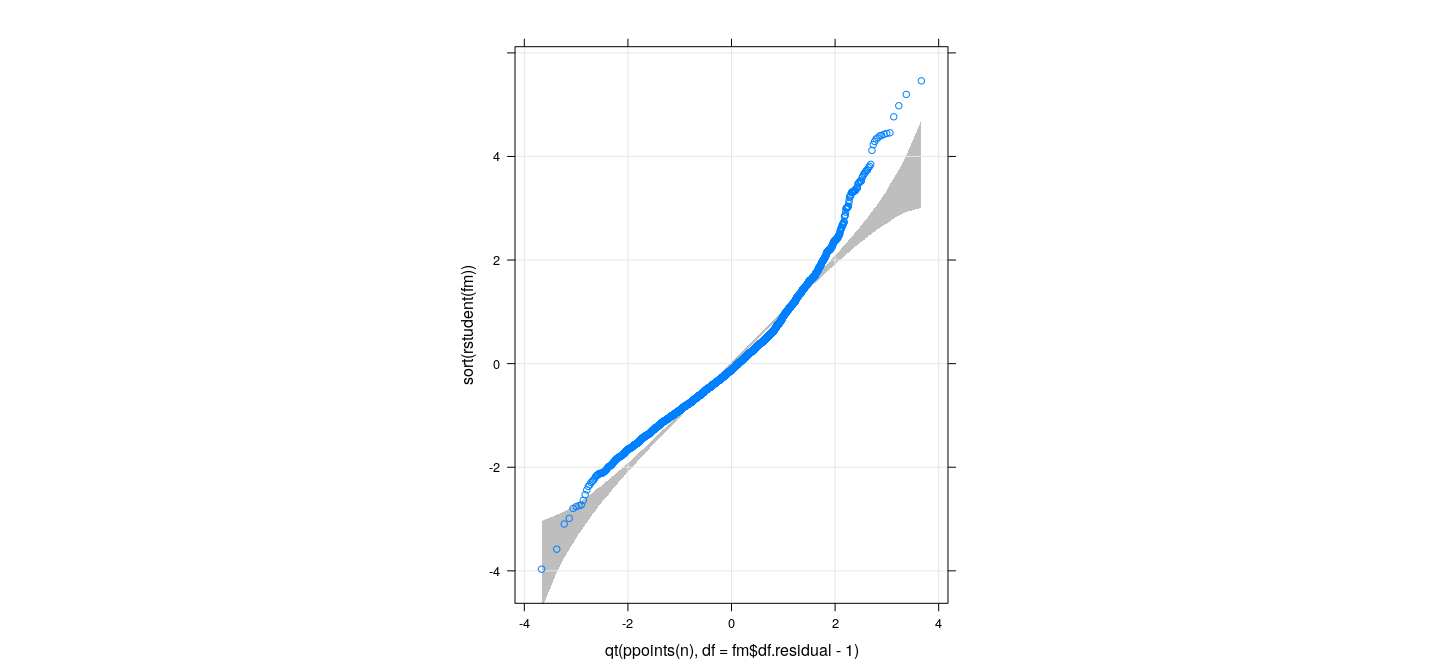

Confidence bounds for QQ-plots using Parametric Bootstrap

Confidence bounds for QQ-plots using Parametric Bootstrap

xyplot(sort(rstudent(fm)) ~ qt(ppoints(n), df = fm$df.residual - 1), grid = TRUE, aspect = "iso") +

layer_(panel.polygon(c(x, rev(x)), c(qsim[1,], rev(qsim[2,])), col = "grey", border = NA))

![plot of chunk unnamed-chunk-4]()

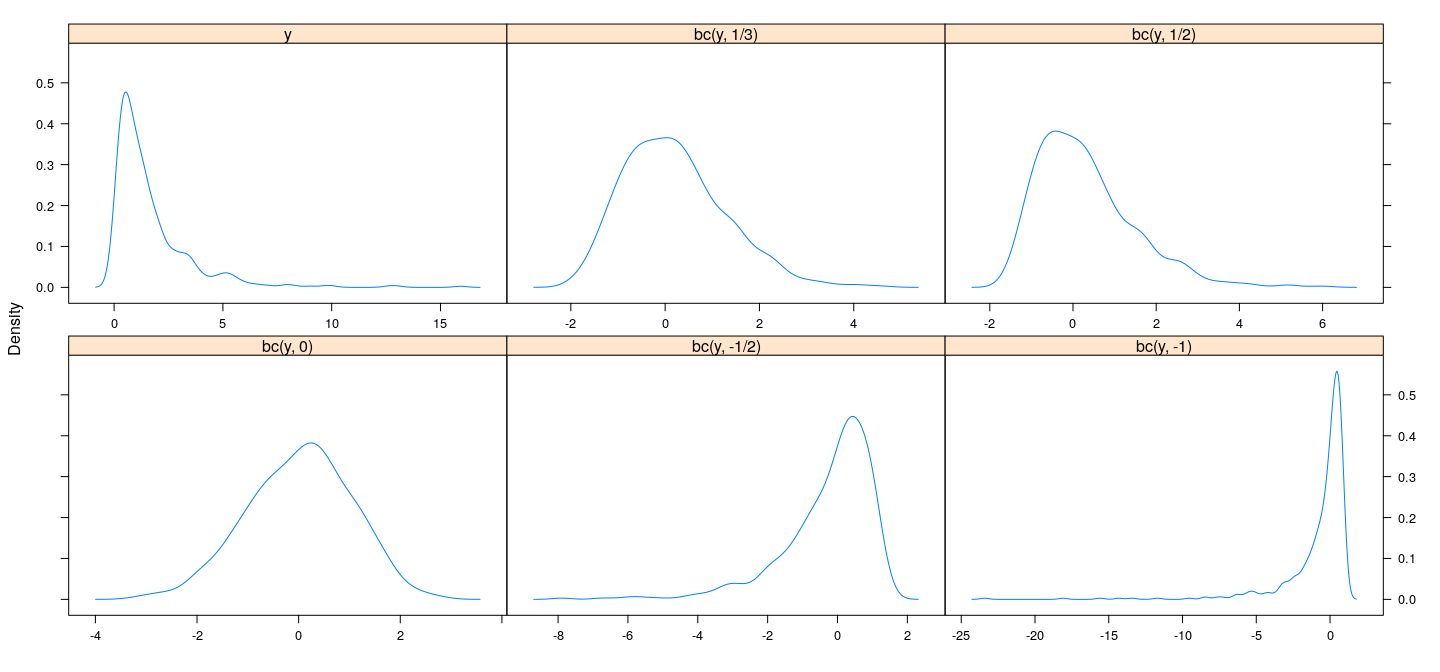

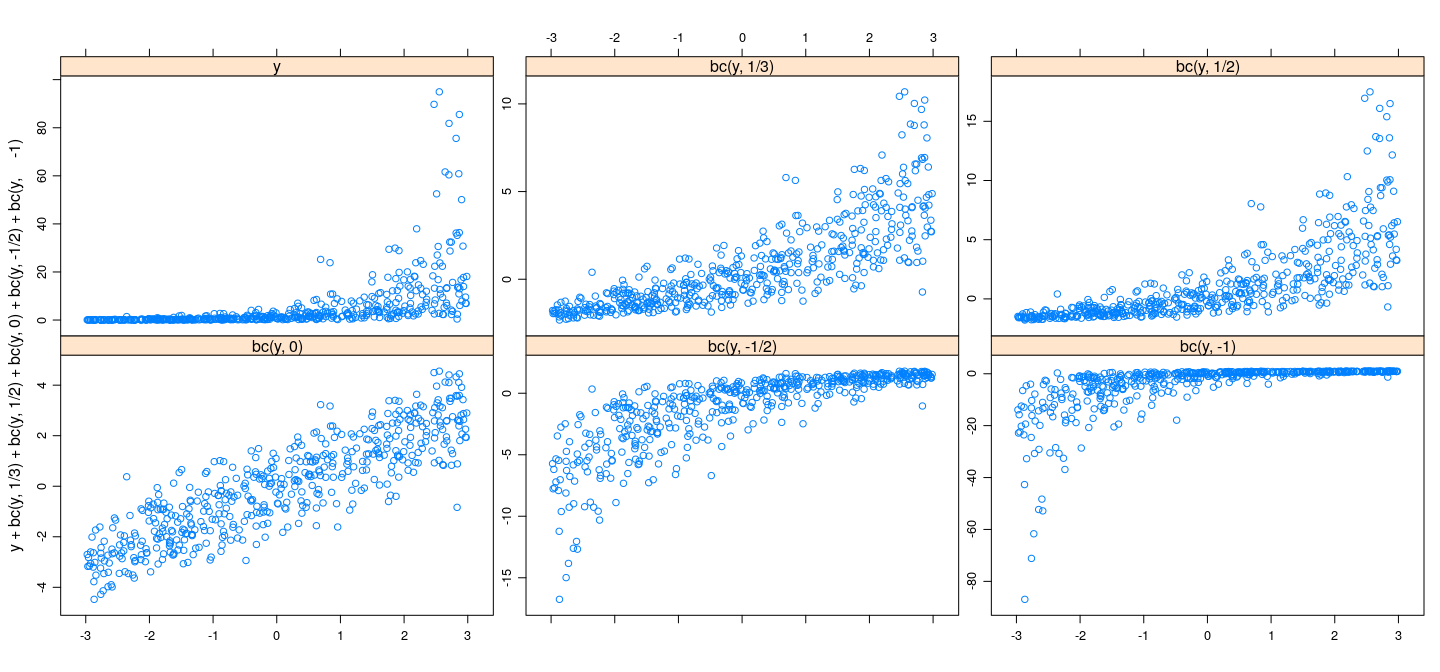

How can we address non-Normality?

Sometimes, a more general model may be appropriate (e.g., GLMs, to be studied later)

Often, transforming the response can prove useful

- E.g., variance stabilizing transformations (depending on distributions)

- \(\sqrt{y}\) for Poisson

- \(\sin^{-1} (\sqrt{y})\) for Binomial

\(\log y\) for positive-valued data (especially economic data)

Logit transform \(\log (p / (1-p))\) for proportions

More details: Kolmogorov-Smirnoff test

\[\hat{F}_n(x) = \frac{1}{n} \sum_i \mathbf{1} \{ X_i \leq x \}\]

\[T(X_1, \dotsc, X_n) = \sup_{x \in \mathbb{R}} \lvert \hat{F}_n(x) - F_0(x) \rvert\]

- Note that

- null distribution of \(T\) does not depend on \(F_0\) (use \(U_i = F_0(X_i) \sim \text{ i.i.d. } U(0, 1)\) instead)

- Intuitively, large value of \(T\) indicates departure from null, so reject when \(T\) is large

- \(p\)-value can be approximated using simulation

- Can also be estimated conservatively using the DKW inequality

More details: Shapiro-Wilk test

Null hypothesis: \(X_1, \dotsc, X_n \sim \text{ i.i.d. } N(\mu, \sigma^2)\) for some \(\mu, \sigma^2\)

Test statistic

\[W = \frac{ (\sum_i a_i X_{(i)})^2 }{\sum_i (X_i - \bar{X})^2}\]

\[\mathbf{a} = \frac{\mathbf{m}^T \mathbf{V}}{\sqrt{\mathbf{m}^T \mathbf{V}^{-1} \mathbf{V}^{-1} \mathbf{m}} }\]

with \(\mathbf{m}\) and \(\mathbf{V}\) the mean vector and variance-covariance matrix of \((Z_{(1)}, \dotsc, Z_{(n)})^T\), where \(Z_1, \dotsc, Z_n \sim \text{ i.i.d. } N(0, 1)\)

The motivation (and implementation) for this test is slightly complicated, but the basic idea is that \(\sum_i a_i X_{(i)}\) estimates the slope of the Normal Q-Q plot (which is an estimate of \(\sigma\)). See Shapiro and Wilk, 1965 for details.

Summary

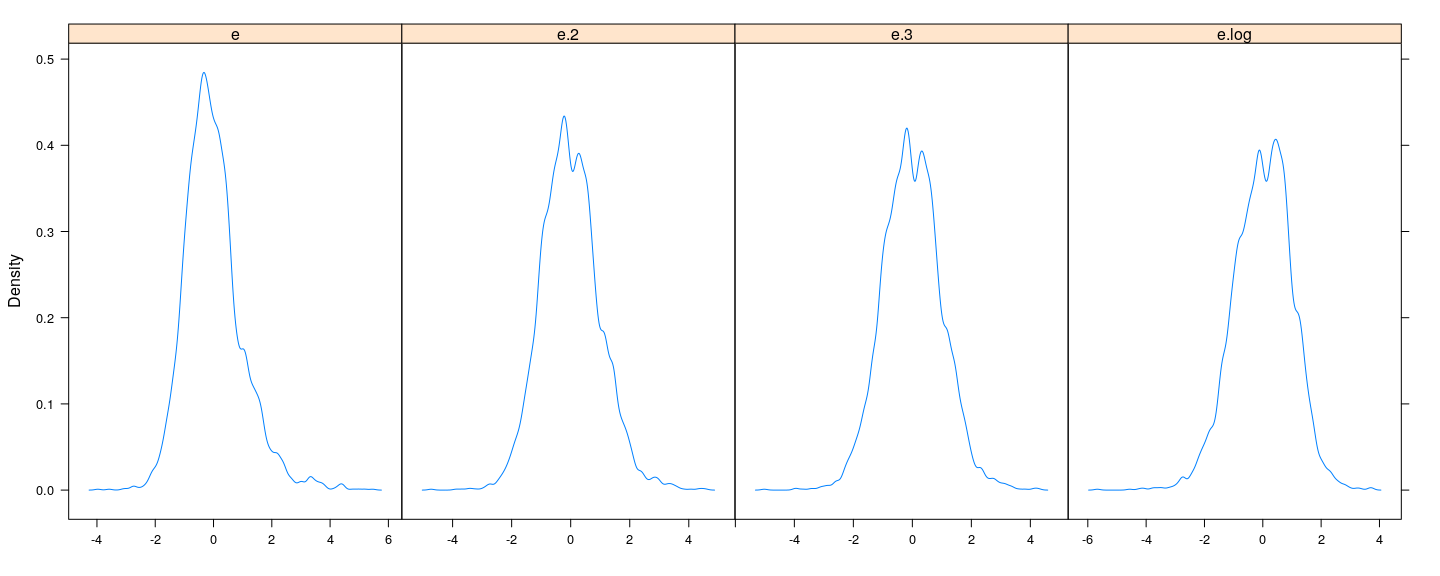

log, square root, cube root all reasonable (graphically)

Formal tests are sometimes too sensitive (especially for large data)

Formal tests useful, but should not be taken too seriously

Nonconstant error variance

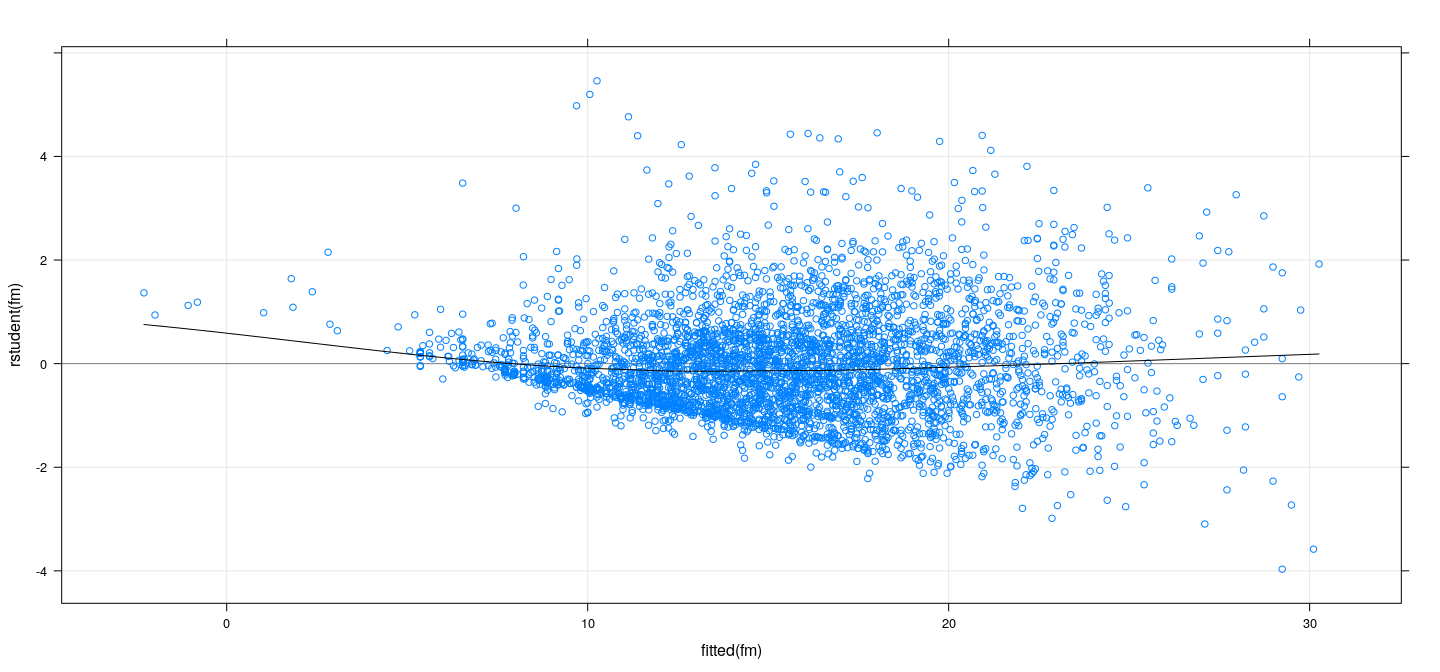

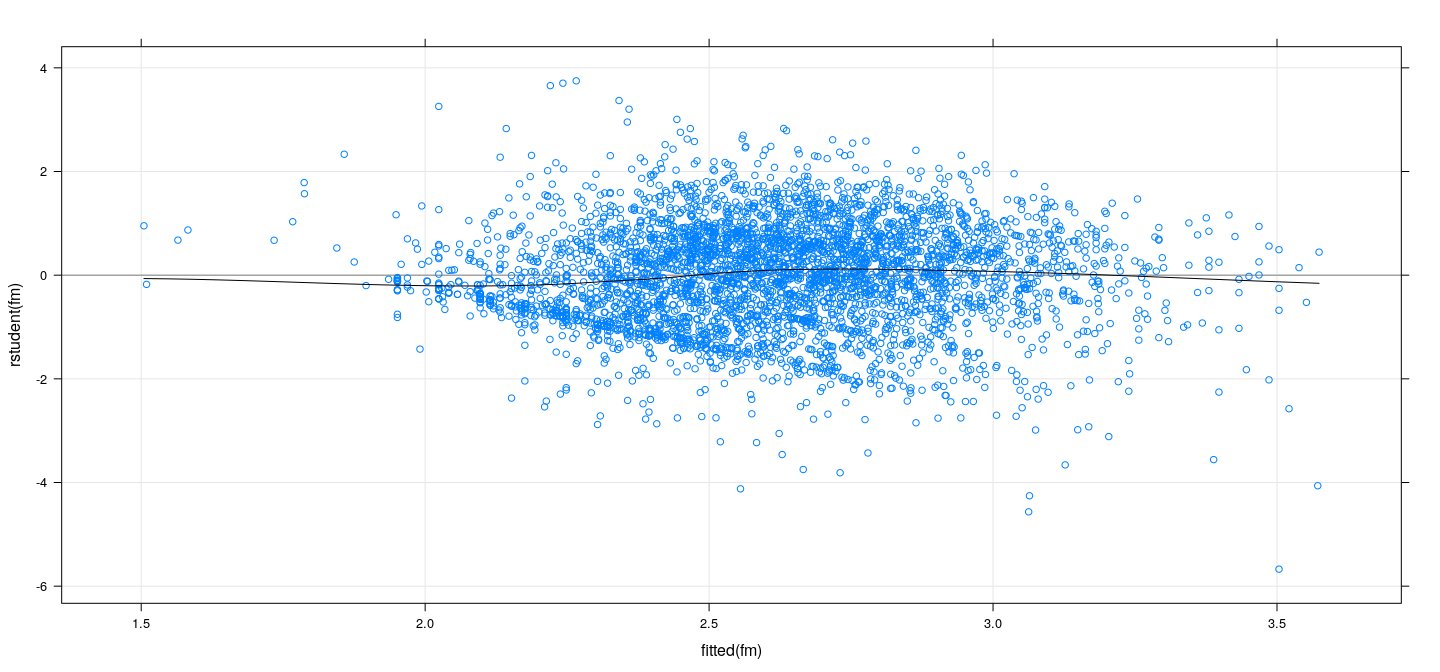

Plotting Residuals vs fitted values

Residuals (\(\mathbf{y} - \hat{\mathbf{y}}\)) are uncorrelated with fitted values (\(\hat{\mathbf{y}}\)) (but not with \(\mathbf{y}\))

Residuals have unequal variances, so preferable to plot Studentized residuals

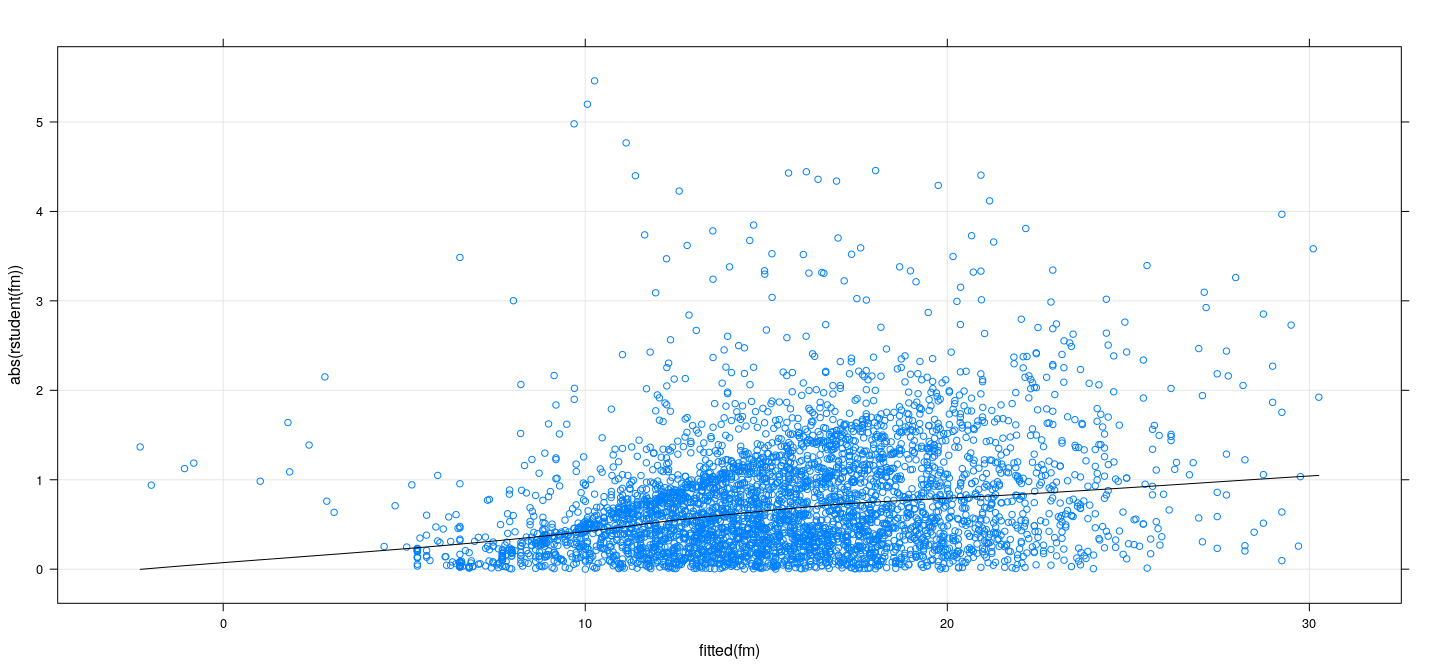

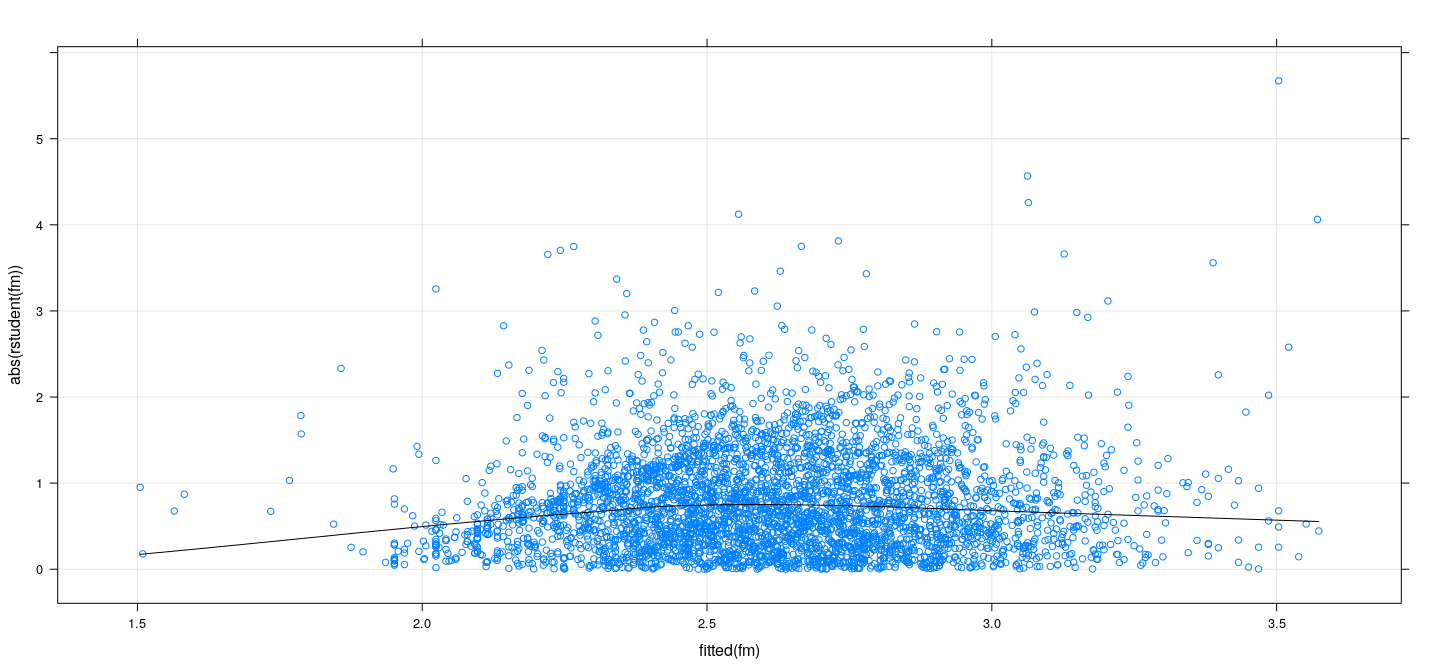

If true error variances depend on \(E(Y | X = x)\), we expect to see the same dependence in plot

More useful to plot absolute Studentized residuals (\(\lvert t_i \rvert\)) along with a non-parametric smoother

Studentized residuals vs fitted values

![plot of chunk unnamed-chunk-11]()

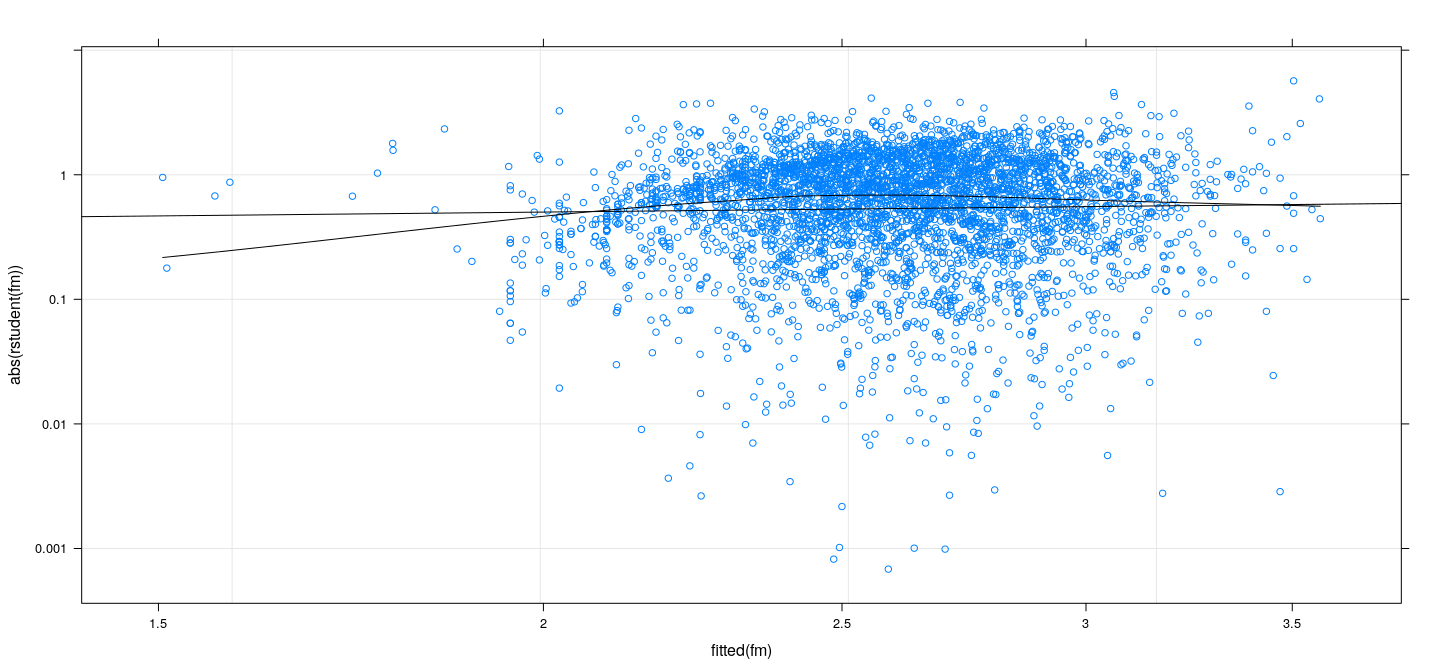

Absolute Studentized residuals vs fitted values

![plot of chunk unnamed-chunk-12]()

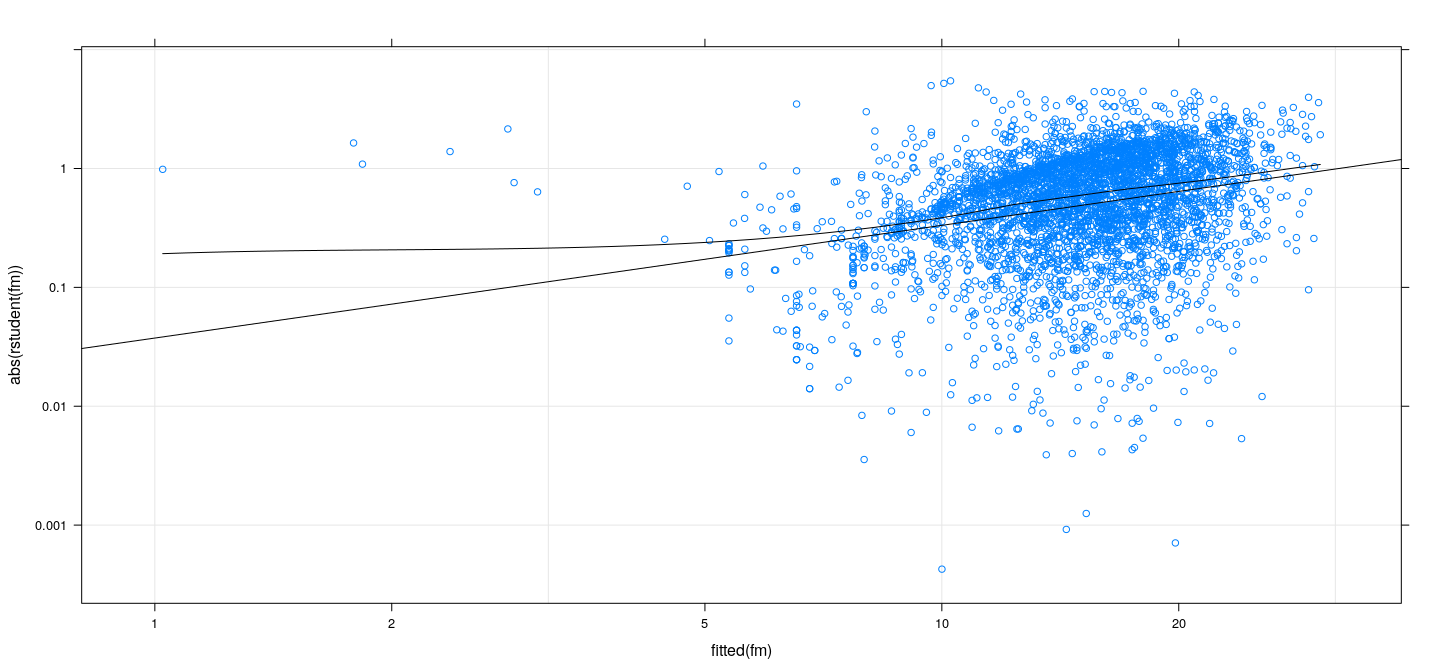

Spread-level plots

Suppose (most) fitted values are positive

We can plot both absolute residuals and fitted values in log scales

A linear relationship in this plot suggests a power transformation

Spread-level plots

![plot of chunk unnamed-chunk-13]()

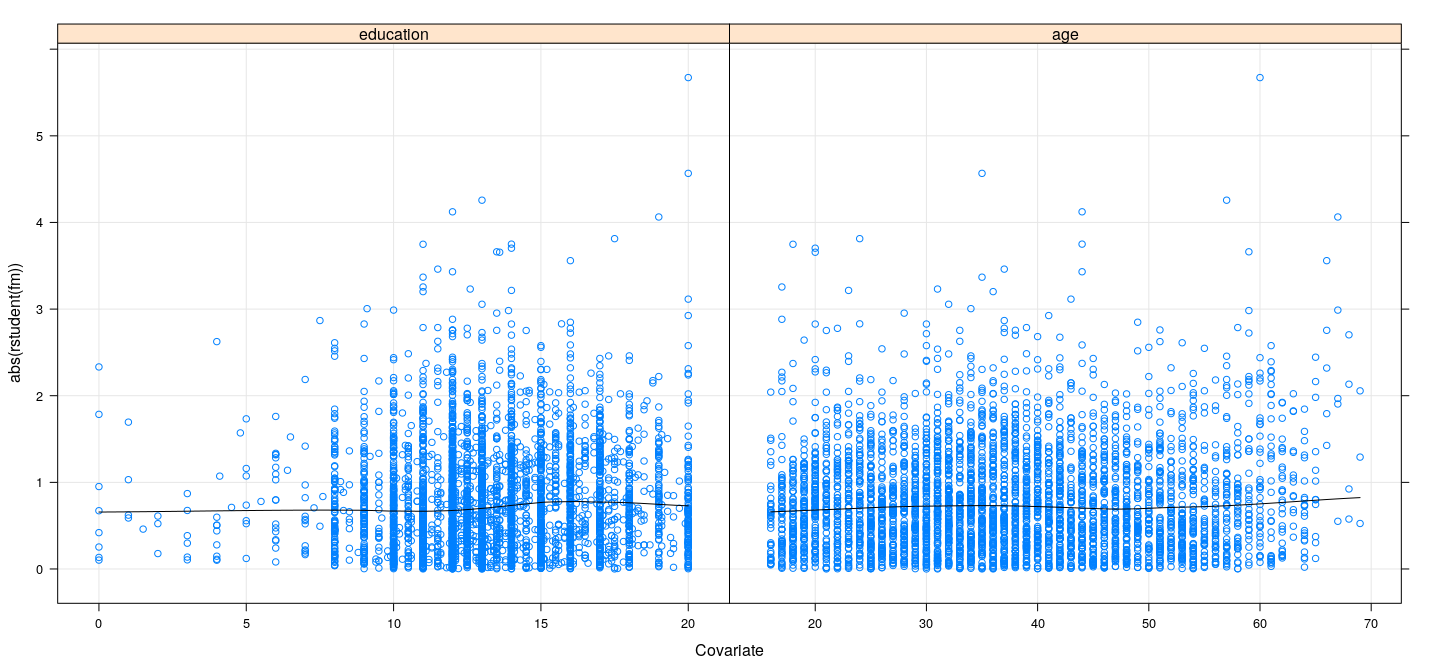

Residuals vs covariates

![plot of chunk unnamed-chunk-18]()

Weighted least-squares estimation

Suppose we can find known weights \(w_i\) such that \(E(y_i | \mathbf{x}_i) = \mathbf{x}_i^T \mathbf{\beta}\) and \(V(y_i | \mathbf{x}_i) = \sigma^2 / w_i^2\)

Let \(\mathbf{W}\) be a diagonal matrix with entries \(w_i^2\) and \(\mathbf{\Sigma} = \sigma^2 \mathbf{W}^{-1}\). Then

\[

\mathbf{y} \sim N( \mathbf{X} \mathbf{\beta}, \mathbf{\Sigma} )

\]

- The likelihood function is given by

\[\begin{align}

L(\mathbf{\beta}, \sigma^2) &=& \frac{1}{(2\pi)^{n/2} \lvert \mathbf{\Sigma} \rvert^{1/2}} \exp \left[ -\frac12 (\mathbf{y} - \mathbf{X} \beta)^T \mathbf{\Sigma}^{-1} (\mathbf{y} - \mathbf{X} \beta) \right] \\

&=& \frac{1}{(2\pi \sigma^2)^{n/2} \lvert \mathbf{W} \rvert^{1/2}} \exp \left[ -\frac1{2\sigma^2} \sum_{i=1}^n w_i^2 (y_i - \mathbf{x}_i^T \beta)^2 \right]

\end{align}\]

Weighted least-squares estimation

- Maximum likelihood estimators are easily seen (exercise) to be given by

\[

\hat{\mathbf{\beta}} = (\mathbf{X}^T \mathbf{W} \mathbf{X})^{-1}

\mathbf{X}^T \mathbf{W} \mathbf{y}\,,\quad

\hat{\sigma}^2 = \frac1{n} \sum w_i^2 (y_i - \mathbf{x}_i^T \hat{\mathbf{\beta}})^2

\]

- In R,

lm() supports weighted least squares through the weights argument

Effect of non-constant variance on OLS estimates

Let \(E(\mathbf{y}) = \mathbf{X} \beta\) and \(V(\mathbf{y}) = \mathbf{\Sigma} = diag\{ \sigma_1^2, \dotsc, \sigma_n^2 \}\)

Suppose we ignore non-constant variance and estimate \(\beta\) using OLS.

\(\hat\beta\) is still unbiased:

\[E(\hat\beta) = (\mathbf{X}^T\mathbf{X})^{-1} \mathbf{X}^T E(\mathbf{y}) = (\mathbf{X}^T\mathbf{X})^{-1} \mathbf{X}^T \mathbf{X} \beta = \beta\]

\[V(\hat\beta) = (\mathbf{X}^T\mathbf{X})^{-1} \mathbf{X}^T \mathbf{\Sigma} \mathbf{X} (\mathbf{X}^T\mathbf{X})^{-1}\]

\[V(\ell^T \hat\beta) = \ell^T (\mathbf{X}^T\mathbf{X})^{-1} \mathbf{X}^T \mathbf{\Sigma} \mathbf{X} (\mathbf{X}^T\mathbf{X})^{-1} \ell\]

- WLS may not be worth the effort if more or less same as OLS standard error

Detecting need for addressing non-constant variance

How can we quickly assess need for WLS?

Suppose we don’t know structural form of \(\mathbf{\Sigma}\) (e.g., which covariates affect variance)

We still know that \(E(\varepsilon_i^2) = \sigma_i^2\)

Natural estimate of \(\sigma_i^2\) after fitting OLS model: \(e_i^2\) or \(e_{i(-i)}^2\), giving \(\hat{\mathbf{\Sigma}}\)

This gives White’s “sandwich estimator”

\[\hat{V}(\hat\beta) = (\mathbf{X}^T\mathbf{X})^{-1} \mathbf{X}^T \hat{\mathbf{\Sigma}} \mathbf{X} (\mathbf{X}^T\mathbf{X})^{-1}\]

How does this help?

We have two alternative estimates of \(V(\hat\beta)\): the OLS and the sandwich estimator

Can obtain corresponding standard errors for \(\ell^T \hat{\beta}\) (in particular for \(t\)-tests for \(\beta_j\)-s)

General strategy:

- If the standard errors using the two methods are substantially similar, OLS is sufficient

- Otherwise, need to address non-constant variance

- This does not suggest any particular remedy: usual approach is to try transformations

How does this help?

Call:

lm(formula = log(wages) ~ education + age + sex, data = SLID)

Residuals:

Min 1Q Median 3Q Max

-2.36252 -0.27716 0.01428 0.28625 1.56588

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.1168632 0.0385480 28.97 <2e-16 ***

education 0.0552139 0.0021891 25.22 <2e-16 ***

age 0.0176334 0.0005476 32.20 <2e-16 ***

sexMale 0.2244032 0.0132238 16.97 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.4187 on 4010 degrees of freedom

Multiple R-squared: 0.3094, Adjusted R-squared: 0.3089

F-statistic: 598.9 on 3 and 4010 DF, p-value: < 2.2e-16

How does this help?

(Intercept) education age sexMale

(Intercept) 1.485945e-03 -6.903578e-05 -1.278690e-05 -9.428603e-05

education -6.903578e-05 4.792018e-06 1.275037e-07 7.454834e-07

age -1.278690e-05 1.275037e-07 2.999080e-07 -7.403851e-08

sexMale -9.428603e-05 7.454834e-07 -7.403851e-08 1.748681e-04

(Intercept) education age sexMale

0.0385479539 0.0021890678 0.0005476385 0.0132237691

How does this help?

(Intercept) education age sexMale

(Intercept) 1.493908e-03 -7.018477e-05 -1.374008e-05 -7.108659e-05

education -7.018477e-05 4.946819e-06 1.370821e-07 6.523566e-07

age -1.374008e-05 1.370821e-07 3.420460e-07 -7.115594e-07

sexMale -7.108659e-05 6.523566e-07 -7.115594e-07 1.750330e-04

(Intercept) education age sexMale

0.038651104 0.002224144 0.000584847 0.013230005

How does this help?

(Intercept) education age sexMale

(Intercept) 1.499263e-03 -7.045519e-05 -1.378453e-05 -7.136218e-05

education -7.045519e-05 4.964996e-06 1.377771e-07 6.614334e-07

age -1.378453e-05 1.377771e-07 3.430706e-07 -7.121512e-07

sexMale -7.136218e-05 6.614334e-07 -7.121512e-07 1.753998e-04

(Intercept) education age sexMale

0.0387203216 0.0022282270 0.0005857223 0.0132438591

Nonlinearity

Non-linearity means the modeled expectation \(E(\mathbf{y}) = \mathbf{X} \beta\) is not adequate

In multiple regression, with many predictors, this may be difficult to detect

Usual strategy: look for indicative patterns in residuals for one predictor at a time

Simplest option is to plot residuals against predictor

But this may not be able to distinguish between monotone and non-monotone relationships

Important to do so because monotone nonlinearity can often be corrected using transformation

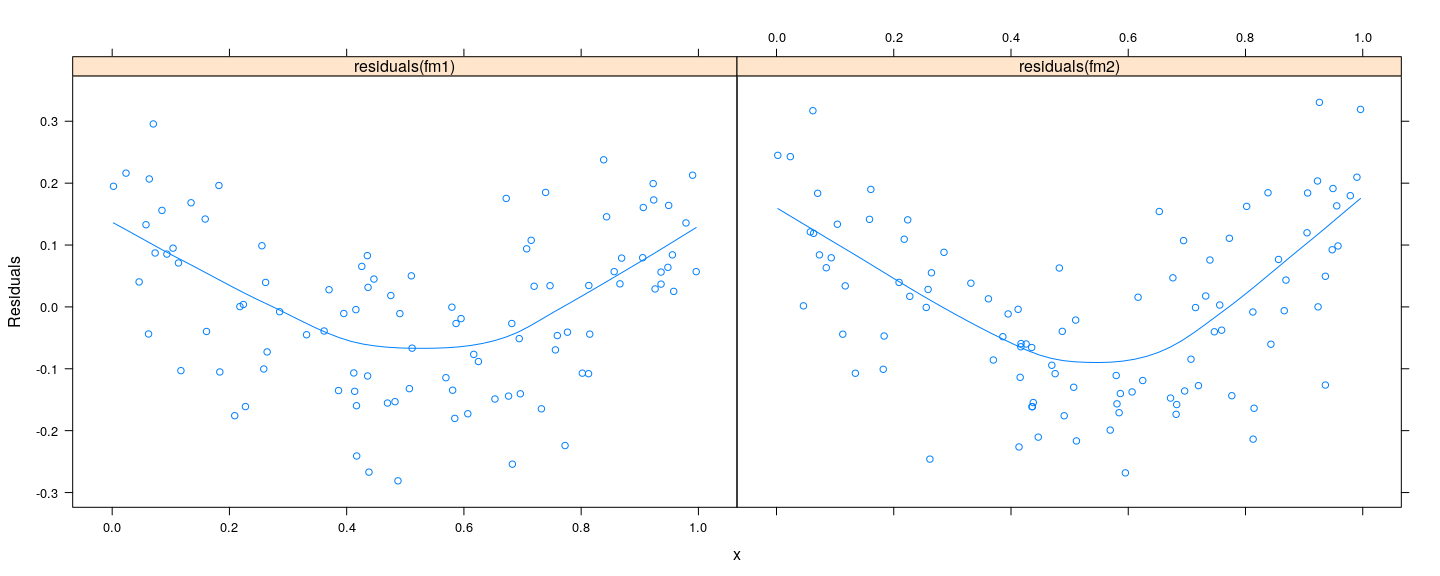

Residual vs covariate: example

![plot of chunk unnamed-chunk-25]()

Residual vs covariate: example

- Similar residual plots, but nature of models are different

- First model can be made linear by transformation (true model: \(y = \alpha + \beta x^2 + \varepsilon\))

- Second model is truly quadratic ((true model: \(y = \alpha + \beta x + \gamma x^2 + \varepsilon\))

![plot of chunk unnamed-chunk-26]()

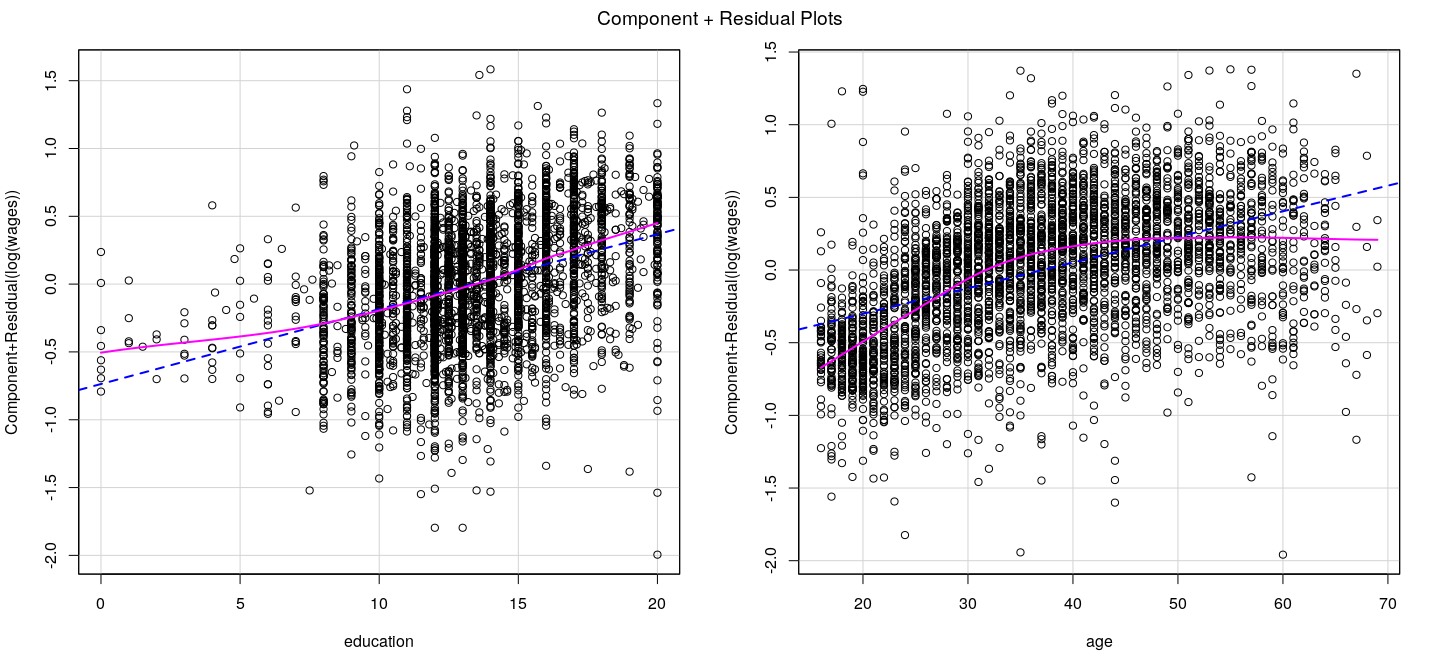

Component plus residual plots

X-axis: \(j\)-th covariate (more accurately, \(j\)-th column of \(\mathbf{X}\))

Y-axis: partial residuals of \(\mathbf{y}\) on \(\mathbf{X}\) excluding \(j\)-th column:

\[e_i^{(-j)} = e_i + \hat{\beta}_j X_{ij}\]

In other words, add back the contribution of the \(j\)-th covariate

Similar to added-variable plots, but covariate is not adjusted

Add non-parametric smoother to detect non-linearity

Component plus residual plots: example

![plot of chunk unnamed-chunk-27]()

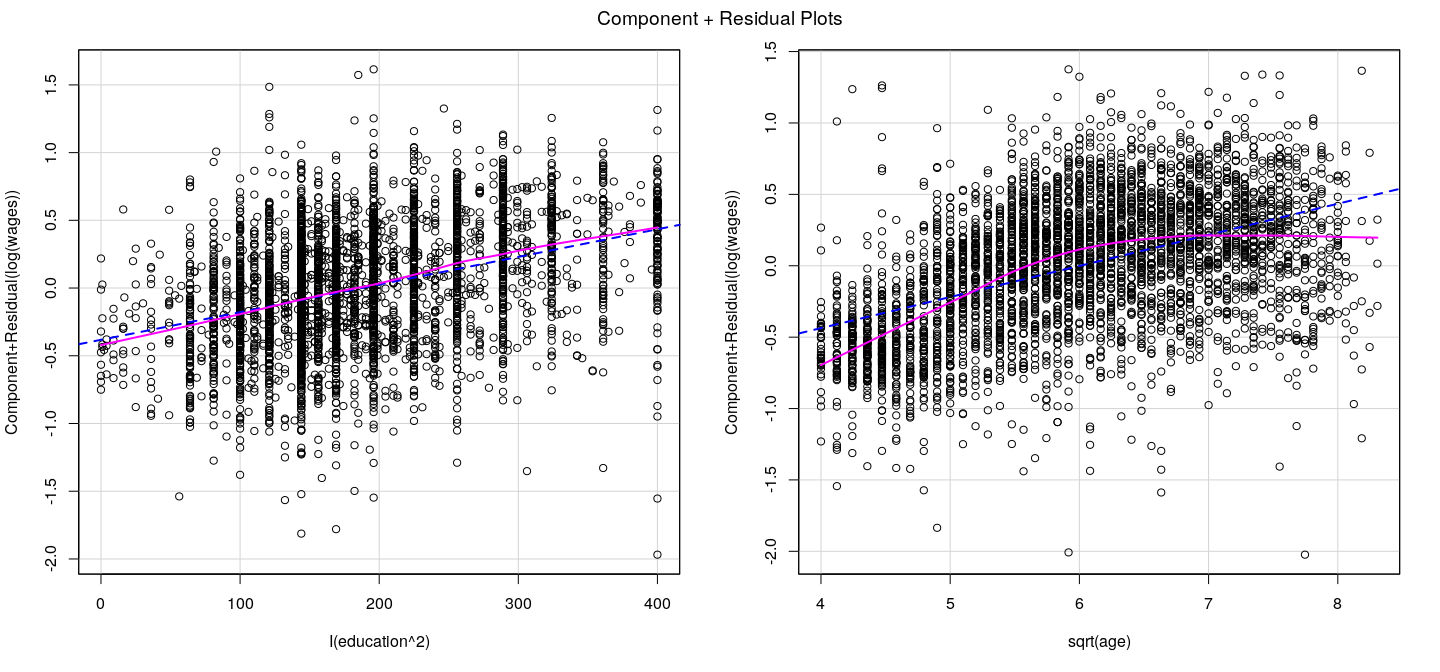

Component plus residual plots: example

![plot of chunk unnamed-chunk-28]()

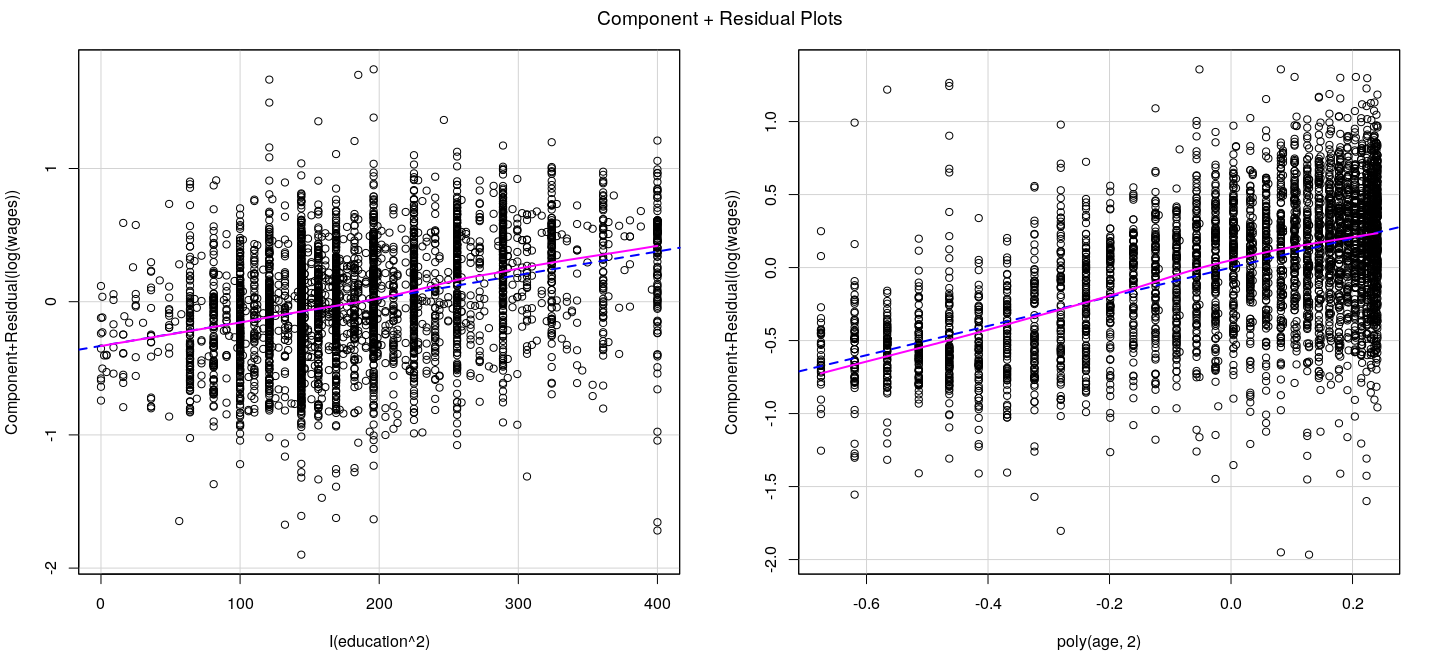

Component plus residual plots: example

![plot of chunk unnamed-chunk-29]()

Component plus residual plots: caveats

Higher dimensional relationships in multiple regression models can be complicated

Component plus residual plots are two dimensional projections

May not always work: in particular, if covariates are non-linearly related

See Mallows (1986) for an approach that accounts for quadratic relationships with other covariates

See Cook (1993) for a more general approach (CERES plots)

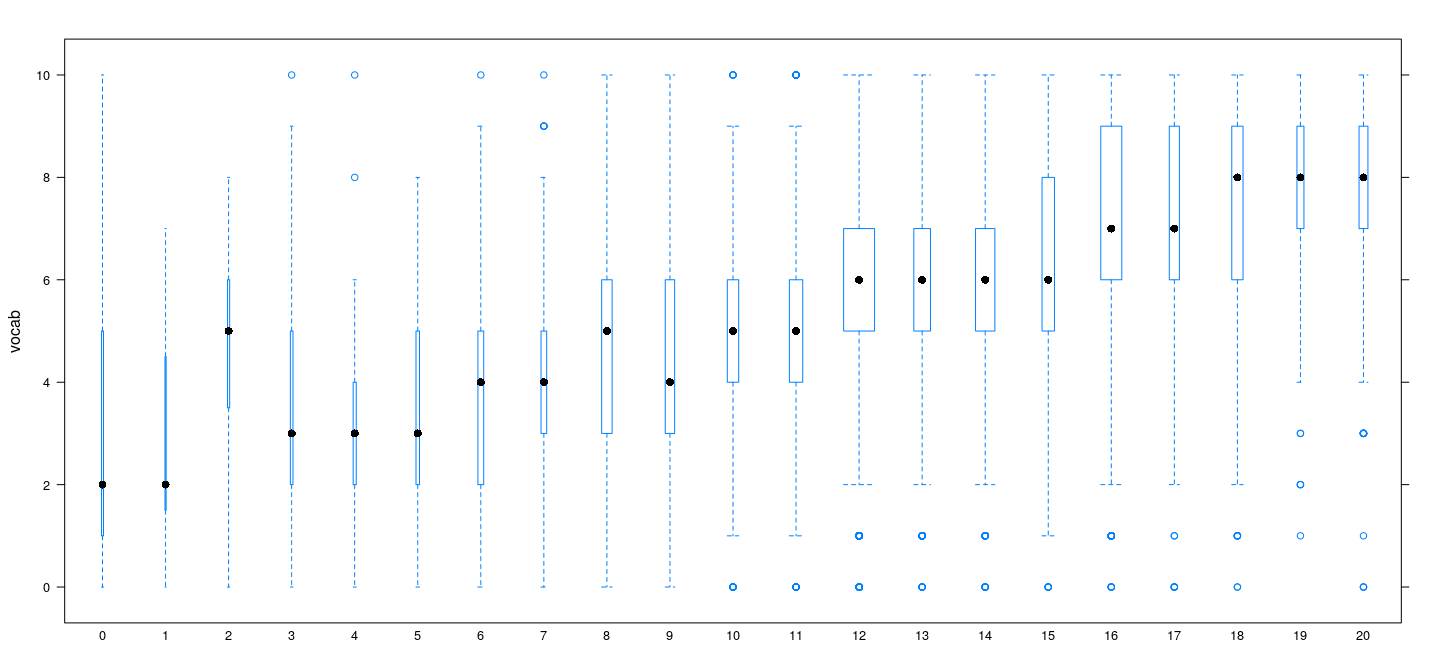

Nonlinearity for discrete predictors

As discussed earlier, discrete covariates (few unique values, many ties) allow us to fit “pure error” models

Pure error models represent a model with no restrictions on the mean function \(f(x) = E(Y | X = x)\)

Can be used to test “lack of fit” for any more specific form of \(f(x)\)

- Example:

GSSvocab (28867 observations)

- Response:

vocab (Number of words out of 10 correct on a vocabulary test)

- Predictors:

age (in years) and educ (years of education)

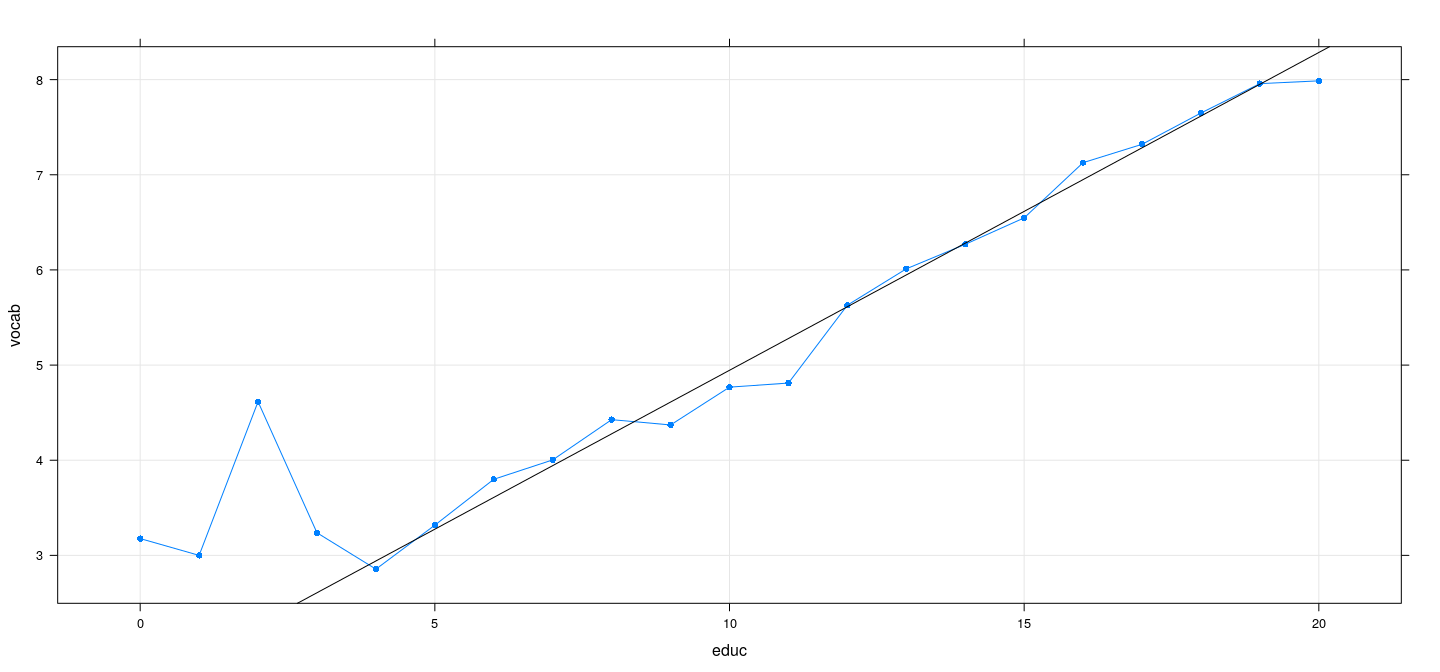

Example: GSSvocab data

![plot of chunk unnamed-chunk-30]()

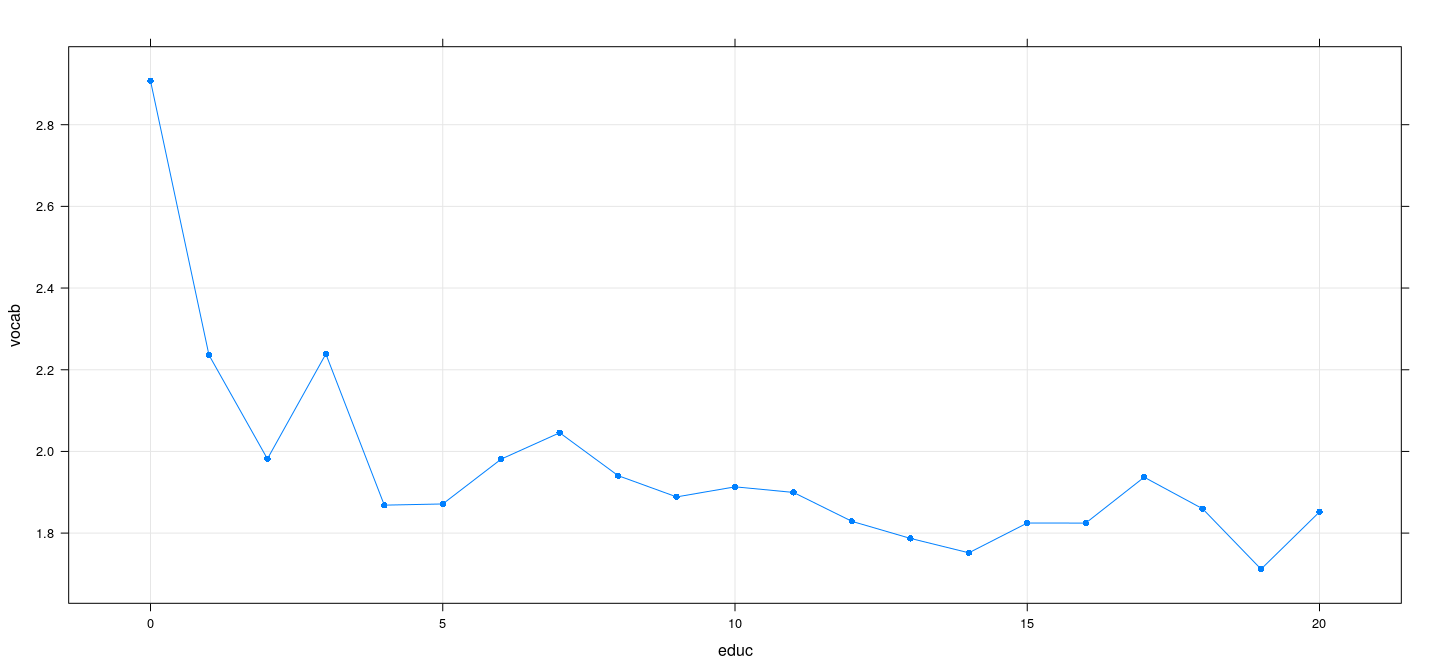

Example: GSSvocab data

![plot of chunk unnamed-chunk-31]()

Example: GSSvocab data

Analysis of Variance Table

Model 1: vocab ~ educ

Model 2: vocab ~ factor(educ)

Res.Df RSS Df Sum of Sq F Pr(>F)

1 27471 93895

2 27452 92906 19 989.32 15.386 < 2.2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Example: GSSvocab data

- Even though there is significant lack of fit, the improvement is marginal

[1] 0.2283162

[1] 0.236447

- This is a common theme

- Statistical tests are more sensitive for large \(n\)

- Statistical significance does not necessarily mean the difference (effect) is important in practice

Example: SLID data

- We can do similar tests for multiple regression models

- \(R^2\) does not improve substantially

$fm1

[1] 0.384718

$fm2

[1] 0.4086884

$fm3

[1] 0.3996565

$fm4

[1] 0.423225

Example: SLID data

Analysis of Variance Table

Model 1: log(wages) ~ I(education^2) + poly(age, 2) + sex

Model 2: log(wages) ~ factor(education) + factor(age) + sex

Res.Df RSS Df Sum of Sq F Pr(>F)

1 4009 626.42

2 3834 587.21 175 39.204 1.4627 9.9e-05 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Example: SLID data

Analysis of Variance Table

Model 1: log(wages) ~ factor(education) + poly(age, 2) + sex

Model 2: log(wages) ~ factor(education) + factor(age) + sex

Res.Df RSS Df Sum of Sq F Pr(>F)

1 3885 602.01

2 3834 587.21 51 14.8 1.8947 0.0001394 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Analysis of Variance Table

Model 1: log(wages) ~ I(education^2) + factor(age) + sex

Model 2: log(wages) ~ factor(education) + factor(age) + sex

Res.Df RSS Df Sum of Sq F Pr(>F)

1 3958 611.21

2 3834 587.21 124 23.995 1.2634 0.02743 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Using pure error models to test for non-constant variance

- With discrete predictors, constant variance means within-group sample variances should be similar

\[

S_j^2 = \frac{1}{n_j-1} \sum_{i=1}^{n_j} (y_{ij} - \bar{y}_j)^2, j = 1, \dotsc, k

\]

- Define the pooled variance

\[

S_p^2 = \frac{1}{n-k} \sum_{j=1}^k (n_j - 1) S_j^2, \text{ where } n = \sum_{j=1}^k n_j

\]

- Then Bartlett’s test statistic is (an adjustment of the likelihood ratio test statistic)

\[

T = \frac{(n-k) \log S_p^2 - \sum_{j=1}^k (n_j-1) \log S_j^2 }{1 + \frac{1}{3(k-1)} (\sum_{j=1}^k \frac{1}{n_j - 1} - \frac{1}{n-k})}

\]

- Under the null distribution of constant variance, \(T\) follows a \(\chi^2\) distribution with \((k-1)\) d.f.

Using pure error models to test for non-constant variance

![plot of chunk unnamed-chunk-39]()

Using pure error models to test for non-constant variance

Bartlett test of homogeneity of variances

data: vocab by factor(educ)

Bartlett's K-squared = 78.606, df = 20, p-value = 6.761e-09

Levene's Test for Homogeneity of Variance (center = median)

Df F value Pr(>F)

group 20 5.3673 6.42e-14 ***

27452

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

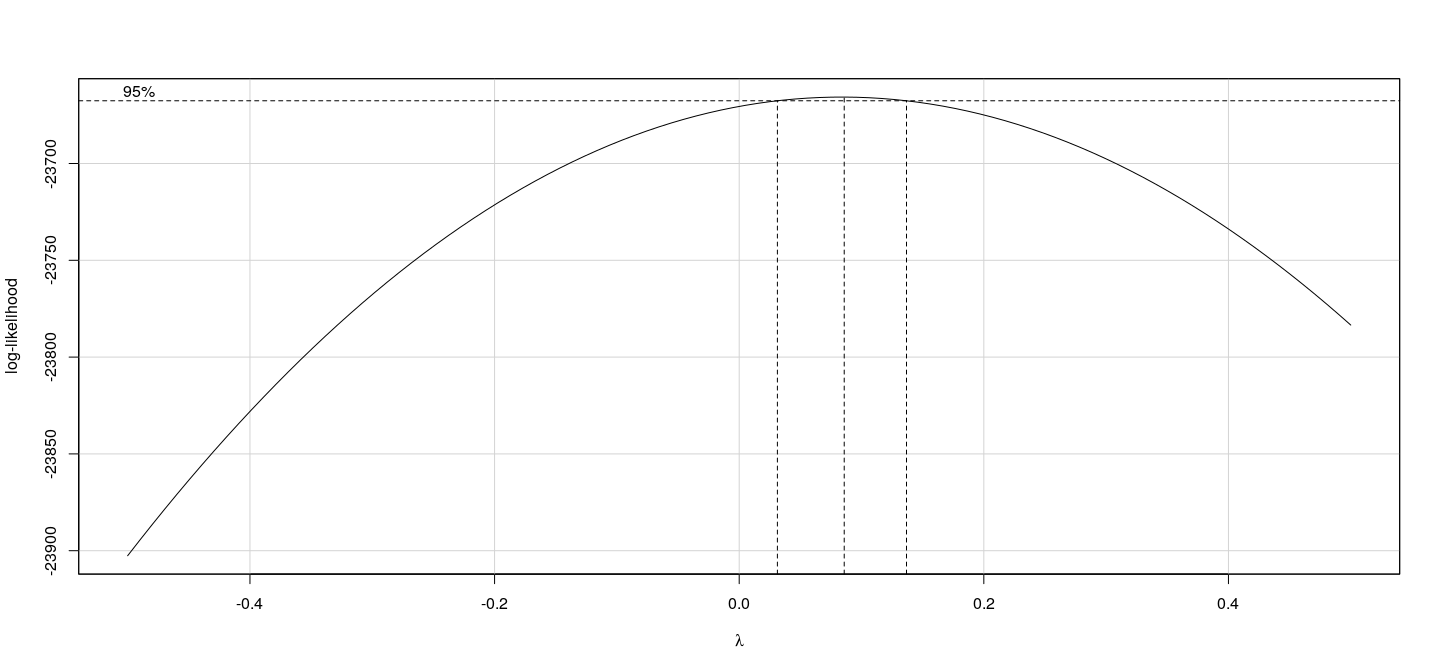

The Box-Tidwell procedure: example

MLE of lambda Score Statistic (z) Pr(>|z|)

I(0.01 + education) 1.8696 4.396 1.103e-05 ***

age -1.6301 -21.772 < 2.2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

iterations = 9